Table of Contents

12

Applications of Computers in Accounting

Computer technology and its usage have registered a significant development during the last three decades. Historically, computers have been used effectively in science and technology to solve the complex computational and logical problems. They have also been used for carrying out economic planning and forecasting processes. Recently, modern day computers have made their presence felt in business and industry. The most important impact of computers has been on the manner in which data is stored and processed within an organisation. Although manual data processing for Management Information System (MIS) has been quite common in the past, modern MIS would be nearly impossible without the use of computer systems. In this chapter we shall discuss the need for the use of computers in accounting, the nature of accounting information system and the types of accounting related MIS reports.

Learning Objectives

After studying this chapter, you will be able to :

• state the meaning, elementsand capabilities of computer system;

• explain the need for computers in accounting;

• describe the automation of accounting process;

• explain design of accounting reports from the accounting data;

• list the various Management Information System (MIS) reports and their uses;

• explain the data interface between information systems.

12.1 Meaning and Elements of Computer System

A computer is an electronic device, which is capable of performing a variety of operations as directed by a set of instructions. This set of instructions is called a computer programme. A computer system is a combination of six elements:

12.1.1 Hardware

Hardware of computer consists of physical components such as keyboard, mouse, monitor and processor. These are electronic and electromechanical components.

12.1.2 Software

A set(s) of programmes, which is used to work with such hardware is called its software. A coded set of instructions stored in the form of circuits is called firmware. There are six types of software as follows:

(a) Operating System : An integrated set of specialised programmes that are meant to manage the resources of a computer and also facilitate its operation is called operating system. It creates a necessary interface that is an interactive link, between the user and the computer hardware.

(b) Utility Programmes : These are a set of computer programmes, which are designed to perform certain supporting operations: such as programme to format a disk, duplicate a disk, physically reorganise stored data and programmes.

(c) Application Software : These are user oriented programmes designed and developed for performing certain specified tasks: such as payroll accounting, inventory accounting, financial accounting, etc.

(d) Language Processors : These are the software, which check for language syntax and eventually translate (or interpret) the source programme (that is a programme written in a computer language) into machine language (that is the language which the computer understands).

(e) System Software : These are a set of programmes which control such internal functions as reading data from input devices, transmitting processed data to output devices and also checking the system to ensure that its components are functioning properly.

(f) Connectivity Software : These are a set of programmes which create and control a connection between a computer and a server so that the computer is able to communicate and share the resources of server and other connected computers.

12.1.3 People

People interacting with the computers are also called live-ware of the computer system. They constitute the most important part of the computer system :

• System Analysts are the people who design data processing systems.

• Programmers are the people who write programmes to implement the data processing system design.

• Operators are the people who participate in operating the computers.

People who respond to the procedures instituted for executing the computer programmes are also a part of live-ware.

12.1.4 Procedures

The procedure means a series of operations in a certain order or manner to achieve desired results. There are three types of procedures which constitute part of computer system: hardware-oriented, software-oriented and internal procedure. Hardware–oriented procedure provide details about components and their method of operation. The software-oriented procedure provides a set of instructions required for using the software of computer system. Internal procedure is instituted to ensure smooth flow of data to computers by sequencing the operation of each sub-system of overall computer system.

12.1.5 Data

These are facts and may consist of numbers, text, etc. These are gathered and entered into a computer system. The computer system in turn stores, retrieves, classifies, organises and synthesises the data to produce information according to a pre-determined set of instructions. The data is, therefore, processed and organised to create information that is relevant and can be used for decision-making.

12.1.6 Connectivity

It is being acknowledged as a sixth element of the computer system. The manner in which a particular computer system is connected to others say through telephone lines, microwave transmission, satellite link, etc. is the element of connectivity.

12.2 Capabilities of Computer System

A computer system possesses some characteristics, which, in comparison to human beings, turn out to be its capabilities. These are as follows ;

Speed : It refers to the amount of time computers takes in accomplishing a task or completes an operation. Computers require far less time than human beings in performing a task. Normally, human beings take into account a second or minute as unit of time. But computers have such a fast operating capability that the relevant unit of time is fraction of a second. Most of the modern computers are capable of performing a 100 million calculations per second and that is why the industry has developed Million Instructions per Second (MIPS) as the criterion to classify different computers according to speed.

Accuracy : It refers to the degree of exactness with which computations are made and operations are performed. One might spend years in detecting errors in computer calculations or updating a wrong record. Most of the errors in Computer Based Information System (CBIS) occur because of bad programming, erroneous data and deviation from procedures. These errors are caused by human beings. Errors attributable to hardware are normally detected and corrected by the computer system itself. The computers rarely commit errors and perform all types of complex operations accurately.

Reliability : It refers to the ability with which the computers remain functional to serve the user. Computers systems are well-adapted to performing repetitive operations. They are immune to tiredness, boredom or fatigue. Therefore, they are more reliable than human beings. Yet there can be failures of computer system due to internal and external reasons. Any failure of the computer in a highly automated industry is unacceptable. Therefore, the companies in such situations provide for back-up facility to swiftly take over operations without loss of time.

Versatility : It refers to the ability of computers to perform a variety of tasks: simple as well as complex. Computers are usually versatile unless designed for a specific application. A general purpose computer is capable of being used in any area of application: business, industry, scientific, statistical, technological, communications and so on. A general purpose computer, when installed in an organisation, can take over the jobs of several specialists because of its versatility. computer system when installed can take over the jobs of all these specialists because of being highly versatile. This further ensures fuller utilisation of its capability.

Storage : It refers to the amount of data a computer system can store and access. The computer systems, besides having instant access to data, have huge capacity to store such data in a very small physical space. A CD-ROM with 4.7” of diameter is capable of storing a large number of books, each containing thousands of pages and yet leave enough space for storing more such material. A typical mainframe computer system is capable of storing and providing online billion of characters and thousands of graphic images.

It is clear from the above discussion that computer capabilities outperform the human capabilities. As a result, a computer, when used properly, will improve the efficiency of an organisation.

12.3 Limitations of a Computer System

In spite of possessing all the above capabilities, computers suffer from the following limitations :

Lack of Commonsense : Computer systems as on date do not possess any common sense because no full-proof algorithm has been designed to programme common sense. Since computers work according to a stored programme(s), they simply lack of commonsense.

Zero IQ : Computers are dumb devices with zero Intelligence Quotient (IQ). They cannot visualise and think what exactly to do under a particular situation, unless they have been programmed to tackle that situation. Computers must be directed to perform each and every action, however, minute it may be.

Lack of Decision-making : Decision-making is a complex process involving information, knowledge, intelligence, wisdom and ability to judge. Computers cannot take decisions on their own because they do not possess all the essentials of decision-making. They can be programmed to take such decisions, which are purely procedure-oriented. If a computer has not been programmed for a particular decision situation, it will not take decision due to lack of wisdom and evaluating faculties. Human beings, on the other hand, possess this great power of decision-making.

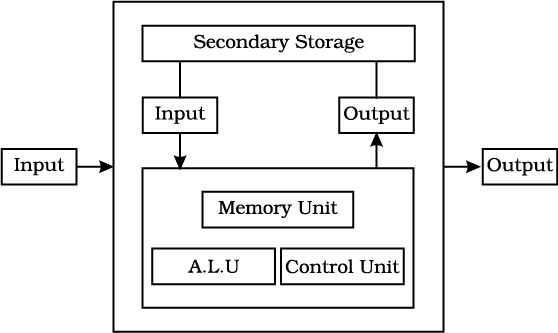

12.4 Components of Computer

The functional components of computer system consist of Input Unit, Central Processing System and Output Unit. The way these components are embedded in a computer may differ from one architectural design to another, yet all of them constitute the essential building blocks of a computer system. Diagrammatically, these components may be presented as follows:

Fig. 12.1 : Block diagram of main components of computer

12.4.1 Input Unit

It controls various input devices which are used for entering data into the computer system. Keyboard and Mouse, for instance, are the most commonly used input device. Other such devices are magnetic tape, magnetic disk, light pen, optical scanner, Magnetic Ink Character (MICR) Recognition, Optical Character Recognition (OCR), bar code reader, smart card reader, etc. Besides, there are other devices which respond to voice and physical touch. A menu layout is displayed on a touch sensitive screen. Whenever user touches a menu item on touch-screen, the computer senses which particular menu item has been touched and accordingly performs the operation associated with that menu item. Such touch screens have been installed at major railway stations for obtaining the online information about arrival and departure of trains.

12.4.2 Central Processing Unit (CPU)

This is the main part of computer hardware that actually processes data, according to the instructions it receives. It controls the flow of data by directing the data to enter the system, places the data into its memory, retrieves the same as and when needed and directs the output of data according to a set of stored instructions. It has three main units as described below :

(a) Arithmetic and Logic Unit (ALU) : It is responsible for performing all the arithmetic computations such as addition, subtraction, division, multiplication and exponentiation. In addition to this, it also performs logical operations involving comparisons among variables and data items.

(b) Memory Unit : In this unit, data is stored before being actually processed. The data so stored is accessed and processed according to a set of instructions which are also stored in the memory of the computer well before such data is transmitted to the memory from input devices.

(c) Control Unit : This unit is entrusted with the responsibility of controlling and coordinating the activities of all other units of the computer system. Specifically, it performs the following functions :

• Read instructions out of memory unit;

• Decode such instructions;

• Set up the routing of data, through internal circuitry/wiring, to the desired place at right time; and

• Determine the input device from where to get next instruction after the instruction in hand has been executed.

12.4.3 Output Unit

After processing the data, the information produced according to a set of instruction need to be made available to user in a human readable and understandable form. A computer system, therefore, needs an output device to communicate such information to the user. Essentially, the output device is assigned the task of translating the processed data from machine coded form to a human readable form. The commonly used output devices include: external devices like monitor also called Visual Display Unit (VDU), printer, graphic plotter for producing graphs, technical drawings and charts and internal devices like magnetic storage devices. Recently, a new device being perfected is the speech synthesiser, which is capable of producing verbal output that sounds like human speech. Information:

12.5 Evolution of Computerised Accounting

Manual system of accounting has been traditionally the most popular method of keeping the records of financial transactions of an organisation. Conventionally, the bookkeeper (or accountant) used to maintain books of accounts such as cash book, journal and ledger so as to prepare a summary of transactions and final accounts manually. The technological innovations led to the development of various machines capable of performing a variety of accounting functions. For example, the popular billing machine was designed to typewrite description of the transaction along with names, addresses of customers. This machine was capable of computing discounts; adding the net total and posting the requisite data to the relevant accounts. The customer’s bill was generated automatically once the operator has entered the necessary information. These machines combined the features of a typewriter and various kinds of calculators.

With substantial increase in the number of transactions, the technology advanced further. With exponential increase in speed, storage and processing capacity, newer versions of these machines evolved. A computer to which they were connected operated these machines. The success of a growing organisation with complexity of transactions tended to depend on resource optimisation, quick decision-making and control. As a result, the maintenance of accounting data on a real-time (or spontaneous) basis became almost essential. Such a system of maintaining accounting records became convenient with the computerised accounting system.

12.5.1 Information and Decisions

An organisation is a collection of interdependent decision-making units that exist to pursue organisational objectives. As a system, every organisation accepts inputs and transforms them into outputs. All organisational systems pursue certain objectives through a process of resource allocation, which is accomplished through the process of managerial decision-making. Information facilitates decisions regarding allocation of resources and thereby assists an organisation in pursuit of its objectives. Therefore, the information is the most important organisational resource. Every medium sized to large organisation has a well-established information system that is meant to generate the information required for decision-making.

With the increasing use of information systems in organisations, Transaction Processing Systems (TPS) have started playing a vital role in supporting business operations. Every transaction processing system has three components: Input, Processing and Output. Since Information Technology (IT) follows the GIGO principle (Garbage in-Garbage out), it is necessary that input to the IT-based information system is accurate, complete and authorised. This is achieved by automating the input. A large number of devices are now available to automate the input process for a TPS.

12.5.2 Transaction Processing System

Transaction Processing Systems (TPS) are among the earliest computerised systems catering to the requirements of large business enterprises. The purpose of a typical TPS is to record, process, validate and store transactions that occur in the various functional areas of a business for subsequent retrieval and usage. A transaction could be internal or external. When a department requisitions material supplies from stores, an internal transaction is said to have occurred. However, when the purchase department purchases materials from a supplier, an external transaction takes place. The scope of financial accounting is confined to external transactions only. TPS involves following steps in processing a transaction. In order to understand these steps, let us consider a case wherein a customer withdraws money using the Automated Teller Machine (ATM) facility, as described below :

• Data Entry : The action data must be entered into the system before it is processed. There are a number of input devices to enter data: Keyboard, mouse, etc. For example, a bank customer operates an ATM facility to make a withdrawal. The actions taken by the customer constitute data, which is processed after validation by the computerised personal banking system.

• Data Validation : It ensures the accuracy and reliability of input data by comparing the same with some predetermined standards or known data. This validation is performed by error detection and error correction procedures. The control mechanism, wherein actual input is compared with the standard, is meant to detect errors while error correction procedures make suggestions for entering correct data input. The Personal Identification Number (PIN) of the customer is validated with the known data. If it is incorrect, a suggestion is made to indicate that the PIN is invalid. After validating the PIN (which is also a part of processing by TPS), the amount of withdrawal being made by the customer is also checked to ensure that it does not exceed a certain limit.

• Processing and Revalidation : The processing of data, representing actions of the ATM user, occurs almost instantaneously in case of the Online Transaction Processing (OLTP) system provided a valid data representing actions of the user has been encountered. This is called check input validity. Revalidation occurs to ensure that the transaction in terms of delivery of money by ATM has been completed. This is called check output validity.

• Storage : Processed actions, as described above, culminate into financial transaction data, which describe the withdrawal of money by a particular customer, are stored in transaction database of Computerised personal banking system. This implies that only valid transactions are stored in the database.

• Information : The stored data is processed using the query facility to produce desired information. A database supported by DBMS is bound to have standard Structured Query Language (SQL) support.

• Reporting : Finally, reports can be prepared on the basis of the required information content according to decision usefulness of report.

A simple computerised accounting system accepts the complete transaction data as input; stores such data in computer storage media (say hard disk) and retrieves the accounting data for processing as and when required for generating an accounting report, as output. The input-process-output diagram shown below indicates as to how accounting software translates data into information. This processing of data is accomplished either through Batch Processing or Real-time Processing.

Batch Processing applies to large and voluminous data that is accumulated offline from various units: branches or departments. The entire accumulated data is processed in one shot to generate the desired reports according to decision requirement.

Real-Time Processing provides online outcome in the form of information and reports without time lag between the transaction and its processing. The accounting reports are generated by query language popularly called Structured Query Language (SQL). It allows the user to retrieve report relevant information that is capable of being laid out in pre-designed accounting report.

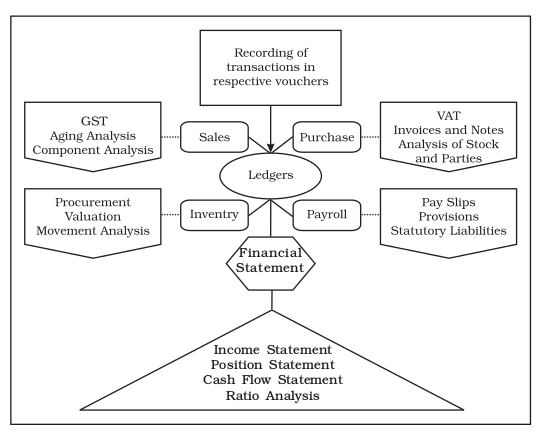

Accounting software may be structured with such components as provide for storage and processing of data pertaining to purchase, sales, inventory, payroll and other financial transactions (refer figure 12.2).

12.6 Features of Computerised Accounting System

Accounting software is used to implement a computerised accounting system. The computer accounting system is based on the concept of databases. It does away with the concept of creating and maintaining journals, ledger, etc. which are essential while working with manual accounting system. Typicaly computerised accounting system offers the following features :

• Online input and storage of accounting data.

• Printout of purchase and sales invoices.

• Logical scheme for codification of accounts and transactions. Every account and transaction is assigned a unique code.

• Grouping of accounts is done from the very beginning.

• Instant reports for management, for example – Aging Statement, Stock Statement, Trial Balance, Trading and Profit and Loss Account, Balance Sheet, Stock Valuation, GST, Returns, Payroll Report, etc.

Fig. 12.2 : Components of computerised accounting software system

Test Your Understanding - I

Fill in the correct words :

1. The user oriented programmes designed and developed for performing certain specific tasks are called as ...........

2. Language syntax is checked by software called as ...........

3. The people who write programmes to implement the data processing system design are called as ...........

4. ...........is the brain of the computer.

5. ...........and ...........are two of the important requirements of an accounting report.

6. An example of responsibility report is ...........

12.7 Management Information System and Accounting

Information System

In order to remain competitive, organisations depend heavily on Information Systems. Management Information System (MIS) is used the most common form of information system. A management information system (MIS) is a system that provides the information necessary to take decisions and manage an organisation effectively. MIS is supportive of the institution’s long-term strategic goals and objectives. MIS is viewed and used at many levels by management: Operational, Tactical and Strategic. Accounting Information System (AIS) identifies, collects, processes, and communicates economic information about an entity to a wide variety of users. Such information is organised in a manner that correct decisions can be based on it.

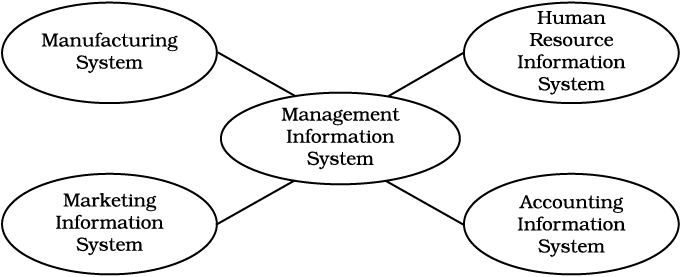

Every accounting system is essentially a part of the Accounting Information System (AIS) which, in turn is a part of the broader system, viz. the organisation’s Management Information System.

The following diagram shows the relationship of the Accounting System with the other functional management information systems.

Fig. 12.3 : Relationship of the accounting system with other functional management information system

The diagram shown above entails the four widely recognised functional areas of management. An organisation operates in a given environment surrounded by the suppliers and customers. The informational needs emerge from the business processes stratified into functional areas where accounting is one of them. The accounting information system (AIS) receives and provides information to the various sub-systems of the institutional/integrated MIS.

Accounting Information System (AIS) is a collection of resources (people and equipment), designed to transform financial and other data into information. This information is communicated to a wide variety of decision-makers. Accepting information systems performs this transformation whether they are essentially manual systems or thoroughly computerised.

Conventionally, MIS was also perceived as day-to-day financial accounting systems that are used to ensure basic control is maintained over financial record keeping activities, but now it is widely recognised as a broader concept and accounting system is a sub component.

The reports generated by the accounting system are disseminated to the various users – internal and external to the organisation. The external parties include the proprietors, investors, creditors, financiers, government suppliers and vendors and the society at large. The reports used by these parties are more of routine nature. However, the internal parties – the employees, managers, etc. use the accounting information for decision-making and control.

12.7.1 Designing of Accounting Reports

Data when processed becomes information. When the related information is summarised to meet a particular need, it is called as a report. The content and design of the report is expected to vary depending upon the level to which it is submitted and decision to made on the basis of the report. A report must be effective and efficient to the user and should substantiate the decision- making process. Akin to any report, every accounting report must be able to fulfil the following criterion :

(a) Relevance

(b) Timeliness

(c) Accuracy

(d) Completeness

(e) Summarisation

The accounting reports generated by the accounting software may be either routine reports or on the specific requirements of the user. For example, the ledger is a routine report while a report on supplies of a particular item by a given party is an on-demand report. However, from a broader perspective, the accounting related MIS reports may be of following reports :

(a) Summary Reports : Summarises all activities of the organisation and present in the form of summary report. Profit and Loss account and Balance Sheet.

(b) Demand Reports : This report will be prepared only when the management requests them, e.g. Bad Debts Report for a given product, Stock Valuation Report.

(c) Customer/Supplier Reports : According to the specifications of the management it will be prepared. For example, Top 10 Customers report, Interest on Customer Account/Invoices, Statement of Account, Customer Reminder Letters Outstanding/Open Delivery Order, Purchase Analysis, Vendor Analysis report.

(d) Exception Reports : According to the conditions or exceptions the report is prepared. For example, Inventory Report in short supplies, Stock Status Query, Over stocked Status, etc.

(e) Responsibility Reports : The MIS structure specifies the premises of management responsibilities. For example, the report on Cash Position, to be submitted by the head of Finance and Accounts department.

The various steps involved in designing accounting reports from accounting data are as follows :

(1) Definition of objectives : the objectives of the report must be clearly defined, who are the users of the report and the decision to be taken on the basis of report.

(2) Structure of the report : the information to be contained therein and the style of presentation.

(3) Querying with the database : the accounting information queries must be clearly defined and the methodology to be adopted while interacting with the database.

(4) Finalising the report.

12.7.2 Data Interface between the Information System

Accounting information system is important component of the organisational MIS in an organisation. It receives information and provides information to the other functional MIS. The following examples illustrate the relationship and data interface between the various sub-components of MIS.

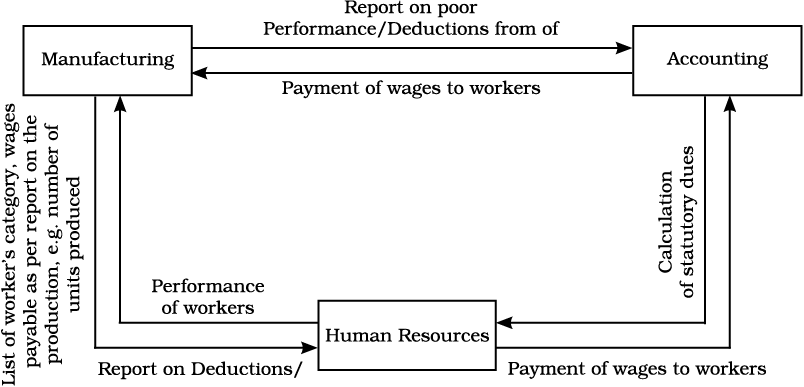

I Accounting Information System, Manufacturing Information System and Human Resource Information System

Look at figure 12.4. It depicts the relationship between the three information systems, viz. manufacturing information system, accounting information system and the human resource information system.

The manufacturing department receives the list of workers from the Human Resource (HR) department. It sends the details of production achieved by the workers on the basis of which the HR department to the finance and accounts (F&A) department to pay the wages. The details of the wages paid and statutory dues are also send by the F & A department to the production department also to the HR department to monitor the performance of workers. The HR department communicates to the other departments about the good/bad performance on the basis decision on various operational matters may be taken.

Fig. 12.4 : Relationship between AIS, manufacturing information system and human resource information system

II AIS and Marketing Information System

Consider the business process in the Marketing and Sales department involving the following activities :

• inquiry

• contact creation

• entry of orders

• dispatch of goods

• billing to customers

The accounting sub-system’s transaction cycle include the processing of sales orders, credit authorisation, custody of the goods, inventory position, shipping information, receivables, etc. It also keeps a track of the customer accounts, e.g. Aging Report, which should be generated by the system.

III AIS and Manufacturing Information System

Similarly, business process in the production department may involve the following activities :

• preparation of plans and schedules

• issue of material requisition forms and job cards

• issue of inventory

• issue of orders for procurement of raw materials

• handling of vendors invoices

• payments to vendors

The accounting sub-system transaction cycle would therefore include the processing of purchase orders, advance to suppliers/vendors, inventory status updation, account payable, etc. All of this information has to share with the other MIS in the organisation.

Hence, the computerised accounting system as a sub component of the accounting information system transforms the financial data into meaningful information and communicates the information to the decision-makers. The report demanded may be routine or specific ones.

Key Terms Introduced in the Chapter

• Operating system

• Management information system

• Analysts

• Transactions processing system

• Utility programme

• Accounting information system

• Data

• Data interface

• Application software

• Report

Summary with Reference to Learning Objectives

1 Meaning of a Computer : Computer is an electronic device capable of performing variety of operations as desired by a set of instructions.

2 Elements of a Computer System :

• Hardware

• Software

• People

• Procedure

• Data

• Connectivity

3 Capabilities of a Computer :

• Speed

• Accuracy

• Reliability

• Versatility

• Storage

4 Need of Computers in Accounting : The advent of globalisation has resulted in the rise in business operations. Consequently, every medium and large sized organisations require well-established information system in order to generate information required for decision-making and achieving the organisational objectives. This made information technology to play vital role in supporting business operations.

5 MIS and Accounting Information System : A management information system provides information necessary to take decisions and manage an organisation effectively. Accounting information system on the other hand identifies, collects, processes and communicates economic information about an entity to a wide variety of users.

6 Accounting Reports : Information supplied to meet a particular need is called report. An accounting report must fulfil the following conditions :

• Relevance

• Timeliness

• Accuracy

• Completeness

• Summarisation

Questions for Practice

Short Answers

1. State the different elements of a computer system.

2. List the distinctive advantages of a computer system over a manual system.

3. Draw block diagram showing the main components of a computer.

4. Give three examples of a transaction processing system.

5. State the relationship between information and decision.

6. What is Accounting Information System?

7. State the various essential features of an accounting report.

8. Name three components of a Transaction Processing System.

9. Give example of the relationship between a Human Resource Information System and MIS.

Long Answers

1. ‘An organisation is a collection of interdependent decision-making units that exists to pursue organisational objectives’. In the light of this statement, explain the relationship between information and decisions. Also explain the role of Transaction Processing System in facilitating the decision-making process in business organisations.

2. Explain, using examples, the relationship between the organisational MIS and the other functional information system in an organisation. Describe how AIS receives and provides information to other functional MIS.

3. ‘An accounting report is essential a report which must be able to fulfil certain basic criteria ‘ Explain? List the various types of accounting reports.

4. Describe the various elements of a computer system and explain the distinctive features of a computer system and manual system.

Checklist to Test Your Understanding

1. Application software

2. Language processor

3. Programmer

4. CPU

5. Timliness, Relevance

6. Cash position, Management responsibility