chapter-6

Cash Flow Statement

Learning Objectives

After studying this chapter, you will be able to :

• state the purpose and preparation of statement of cash flow statement;

• distinguish between operating activities, investing activities and financing activities;

• prepare the statement of cash flows using direct method;

• prepare the cash

flow statement using indirect method.

Till now you have learnt about the financial statements being primarily inclusive of Position Statement (showing the financial position of an enterprise as on a particular date) and Income Statement (showing the result of the operational activities of an enterprise over a particular period). There is also a third important financial statement known as Cash flow statement, which shows inflows and outflows of the cash and cash equivalents. This statement is usually prepared by companies which comes as a tool in the hands of users of financial information to know about the sources and uses of cash and cash equivalents of an enterprise over a period of time from various activities of an enterprise. It has gained substantial importance in the last decade because of its practical utility to the users of financial information.

Financial Statement of companies are prepared following the accounting standards prescribed in the companies Act, 2013. Accounting Standards are notified under section 133 of the Companies Act, 2013 vide Accounting Standards Rules, 2006 and are mandatory in nature. Companies Act, 2013 also specifies that if the accounting standards are not followed, financial statements will not be true and fair, which is a quality of financial statement. Financial Statements are defined in Companies Act, 2013 (Section 2 (40)] and includes Cash Flow Statement prepared in accordance with Accounting Standard- 3 (AS-3)- Cash Flow Statement.

A cash flow statement provides information about the historical changes in cash and cash equivalents of an enterprise by classifying cash flows into operating, investing and financing activities. It requires that an enterprise should prepare a cash flow statement and should present it for each accounting period for which financial statements are presented. This chapter discusses this technique and explains the method of preparing a cash flow statement for an accounting period.

6.1 Objectives of Cash Flow Statement

A Cash flow statement shows inflow and outflow of cash and cash equivalents from various activities of a company during a specific period. The primary objective of cash flow statement is to provide useful information about cash flows (inflows and outflows) of an enterprise during a particular period under various heads, i.e., operating activities, investing activities and financing activities.

This information is useful in providing users of financial statements with a basis to assess the ability of the enterprise to generate cash and cash equivalents and the needs of the enterprise to utilise those cash flows. The economic decisions that are taken by users require an evaluation of the ability of an enterprise to generate cash and cash equivalents and the timing and certainty of their generation.

6.2 Benefits of Cash Flow Statement

Cash flow statement provides the following benefits : A cash flow statement when used along with other financial statements provides information that enables users to evaluate changes in net assets of an enterprise, its financial structure (including its liquidity and solvency) and its ability to affect the amounts and timings of cash flows in order to adapt to changing circumstances and opportunities.

Cash flow information is useful in assessing the ability of the enterprise to generate cash and cash equivalents and enables users to develop models to assess and compare the present value of the future cash flows of different enterprises.

It also enhances the comparability of the reporting of operating performance by different enterprises because it eliminates the effects of using different accounting treatments for the same transactions and events.

It also helps in balancing its cash inflow and cash outflow, keeping in response to changing condition. It is also helpful in checking the accuracy of past assessments of future cash flows and in examining the relationship between profitability and net cash flow and impact of changing prices.

6.3 Cash and Cash Equivalents

As stated earlier, cash flow statement shows inflows and outflows of cash and cash equivalents from various activities of an enterprise during a particular period. As per AS-3, ‘Cash’ comprises cash in hand and demand deposits with banks, and ‘Cash equivalents’ means short-term highly liquid investments that are readily convertible into known amounts of cash and which are subject to an insignificant risk of changes in value. An investment normally qualifies as cash equivalents only when it has a short maturity, of say, three months or less from the date of acquisition. Investments in shares are excluded from cash equivalents unless they are in substantial cash equivalents. For example, preference shares of a company acquired shortly before their specific redemption date, provided there is only insignificant risk of failure of the company to repay the amount at maturity. Similarly, short-term marketable securities which can be readily converted into cash are treated as cash equivalents and is liquidable immediately without considerable change in value.6.4 Cash Flows

‘Cash Flows’ implies movement of cash in and out due to some non-cash items. Receipt of cash from a non-cash item is termed as cash inflow while cash payment in respect of such items as cash outflow. For example, purchase of machinery by paying cash is cash outflow while sale proceeds received from sale of machinery is cash inflow. Other examples of cash flows include collection of cash from trade receivables, payment to trade payables, payment to employees, receipt of dividend, interest payments, etc.

Cash management includes the investment of excess cash in cash equivalents. Hence, purchase of marketable securities or short-term investment which constitutes cash equivalents is not considered while preparing cash flow statement.

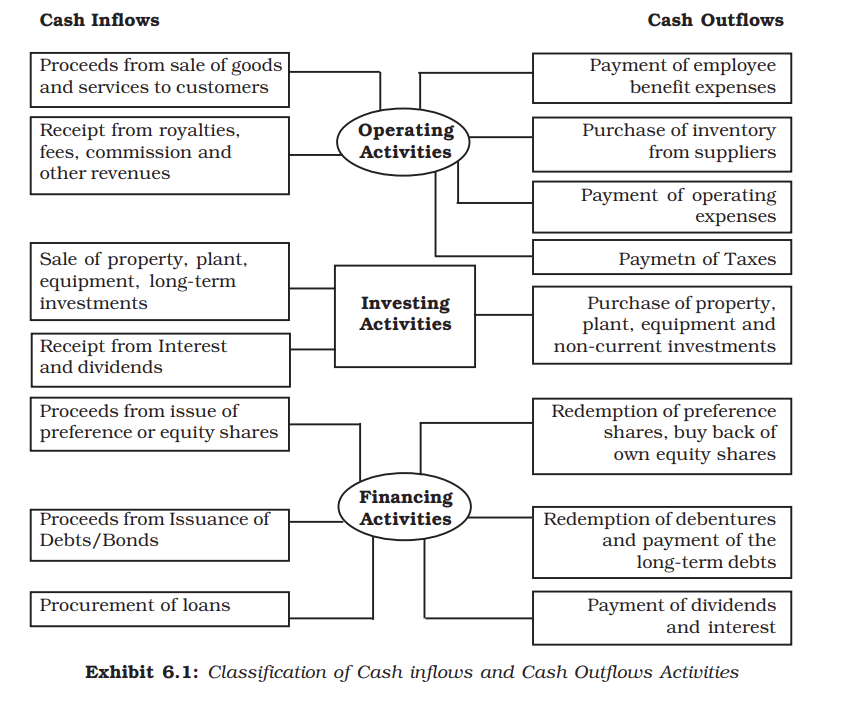

6.5 Classification of Activities for the Preparation of Cash Flow Statement

You know that various activities of an enterprise result into cash flows (inflows or receipts and outflows or payments) which is the subject matter of a cash flow statement. As per AS-3, these activities are to be classified into three categories: (1) operating, (2) investing, and (3) financing activities so as to show separately the cash flows generated (or used) by (in) these activities. This helps the users of cash flow statement to assess the impact of these activities on the financial position of an enterprise and also on its cash and cash equivalents.6.5.1 Cash from Operating Activities

Operating activities are the activities that constitute the primary or main activities of an enterprise. For example, for a company manufacturing garments, operating activities are procurement of raw material, incurrence of manufacturing expenses, sale of garments, etc. These are the principal revenue generating activities (or the main activities) of the enterprise and these activities are not investing or financing activities. The amount of cash from operations’ indicates the internal solvency level of the company, and is regarded as the key indicator of the extent to which the operations of the enterprise have generated sufficient cash flows to maintain the operating capability of the enterprise, paying dividends, making of new investments and repaying of loans without recourse to external source of financing.

Cash flows from operating activities are primarily derived from the main activities of the enterprise. They generally result from the transactions and other events that enter into the determination of net profit or loss. Examples of cash flows from operating activities are:

Cash Inflows from operating activities- cash receipts from sale of goods and the rendering of services.

- cash receipts from royalties, fees, commissions and other revenues.

- Cash payments to suppliers for goods and services.

- Cash payments to and on behalf of the employees.

- Cash payments to an insurance enterprise for premiums and claims, annuities, and other policy benefits.

- Cash payments of income taxes unless they can be specifically identified with financing and investing activities.

The net position is shown in case of operating cash flows.

An enterprise may hold securities and loans for dealing or for trading purposes. In either case they represent Inventory specifically held for resale. Therefore, cash flows arising from the purchase and sale of dealing or trading securities are classified as operating activities. Similarly, cash advances and loans made by financial enterprises are usually classified as operating activities since they relate to main activity of that enterprise.

6.5.2 Cash from Investing Activities

As per AS-3, investing activities are the acquisition and disposal of long-term assets and other investments not included in cash equivalents. Investing activities relate to purchase and sale of long-term assets or fixed assets such as machinery, furniture, land and building, etc. Transactions related to longterm investment are also investing activities.

Separate disclosure of cash flows from investing activities is important because they represent the extent to which expenditures have been made for resources intended to generate future income and cash flows. Examples of cash flows arising from investing activities are:

Cash Outflows from investing activities- Cash payments to acquire fixed assets including intangibles and capitalised research and development.

- Cash payments to acquire shares, warrants or debt instruments of other enterprises other than the instruments those held for trading purposes.

- Cash advances and loans made to third party (other than advances and loans made by a financial enterprise wherein it is operating activities).

- Cash receipt from disposal of fixed assets including intangibles.

- Cash receipt from the repayment of advances or loans made to third parties (except in case of financial enterprise).

- Cash receipt from disposal of shares, warrants or debt instruments of other enterprises except those held for trading purposes.

- Interest received in cash from loans and advances.

- Dividend received from investments in other enterprises.

6.5.3 Cash from Financing Activities

As the name suggests, financing activities relate to long-term funds or capital of an enterprise, e.g., cash proceeds from issue of equity shares, debentures, raising long-term bank loans, repayment of bank loan, etc. As per AS-3, financing activities are activities that result in changes in the size and composition of the owners’ capital (including preference share capital in case of a company) and borrowings of the enterprise. Separate disclosure of cash flows arising from financing activities is important because it is useful in predicting claims on future cash flows by providers of funds ( both capital and borrowings ) to the enterprise. Examples of financing activities are:Cash Inflows from financing activities

- Cash proceeds from issuing shares (equity or/and preference).

- Cash proceeds from issuing debentures, loans, bonds and other short/ long-term borrowings.

Cash Outflows from financing activities

- Cash repayments of amounts borrowed.

- Interest paid on debentures and long-term loans and advances.

- Dividends paid on equity and preference capital.

It is important to mention here that a transaction may include cash flows that are classified differently. For example, when the instalment paid in respect of a fixed asset acquired on deferred payment basis includes both interest and loan, the interest element is classified under financing activities and the loan element is classified under investing activities. Moreover, same activity may be classified differently for different enterprises. For example, purchase of shares is an operating activity for a share brokerage firm while it is investing activity in case of other enterprises.

6.5.4 Treatment of Some Peculiar Items

Extraordinary items

Extraordinary items are not the regular phenomenon, e.g., loss due to theft or earthquake or flood. Extraordinary items are non-recurring in nature and hence cash flows associated with extraordinary items should be classified and disclosed separately as arising from operating, investing or financing activities. This is done to enable users to understand their nature and effect on the present and future cash flows of an enterprise.

Interest and Dividend

In case of a financial enterprise (whose main business is lending and borrowing), interest paid, interest received and dividend received are classified as operating activities while dividend paid is a financing activity.

In case of a non-financial enterprise, as per AS-3, it is considered more appropriate that payment of interest and dividends are classified as financing activities whereas receipt of interest and dividends are classified as investing activities.

Taxes on Income and Gains

Taxes may be income tax (tax on normal profit), capital gains tax (tax on capital profits), dividend tax (tax on the amount distributed as dividend to shareholders). AS-3 requires that cash flows arising from taxes on income should be separately disclosed and should be classified as cash flows from operating activities unless they can be specifically identified with financing and investing activities. This clearly implies that:

- tax on operating profit should be classified as operating cash flows.

- dividend tax, i.e., tax paid on dividend should be classified as financing activity along with dividend paid.

- Capital gains tax paid on sale of fixed assets should be classified under investing activities.

Non-cash Transactions

As per AS-3, investing and financing transactions that do not require the use of cash or cash equivalents should be excluded from a cash flow statement. Examples of such transactions are – acquisition of machinery by issue of equity shares or redemption of debentures by issue of equity shares. Such transactions should be disclosed elsewhere in the financial statements in a way that provide all the relevant information about these investing and financing activities. Hence, assets acquired by issue of shares are not disclosed in cash flow statement due to non-cash nature of the transaction.

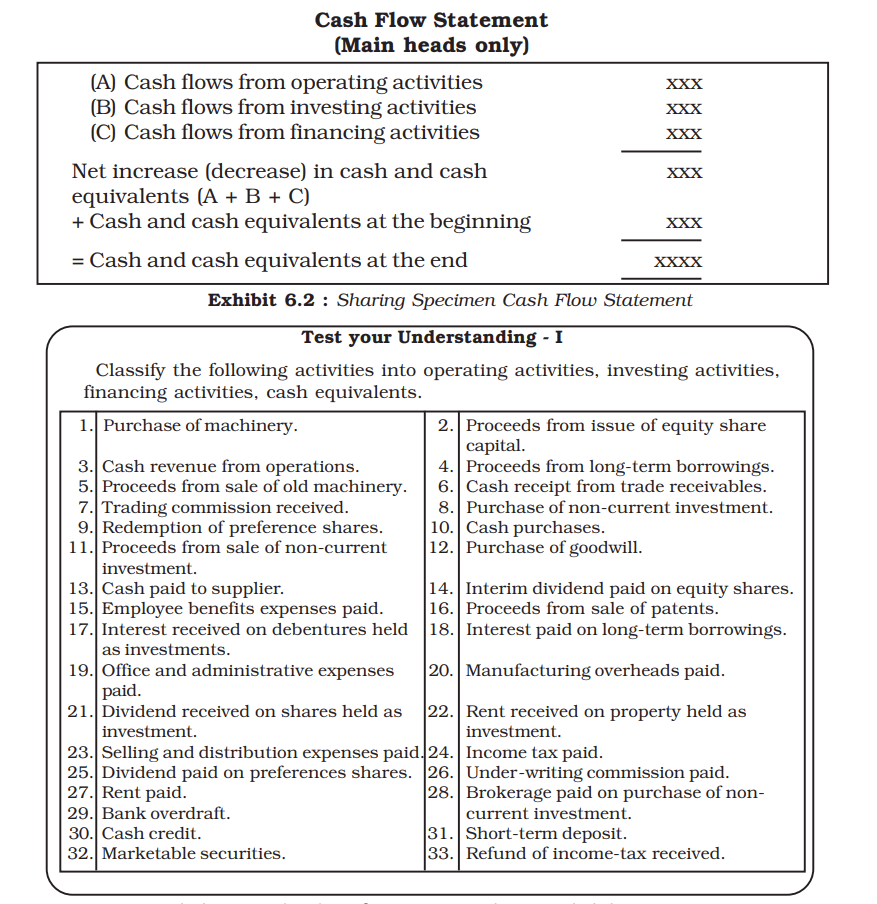

With these three classifications, Cash Flow Statement is shown in Exhibit 6.2.

6.6 Ascertaining Cash Flow from Operating Activities

Operating activities are the main source of revenue and expenditure in an enterprise. Therefore, the ascertainment of cash flows from operating activities need special attention.

As per AS-3, an enterprise should report cash flows from operating activities either by using :

- Direct method whereby major classes of gross cash receipts and gross cash payments are disclosed; or

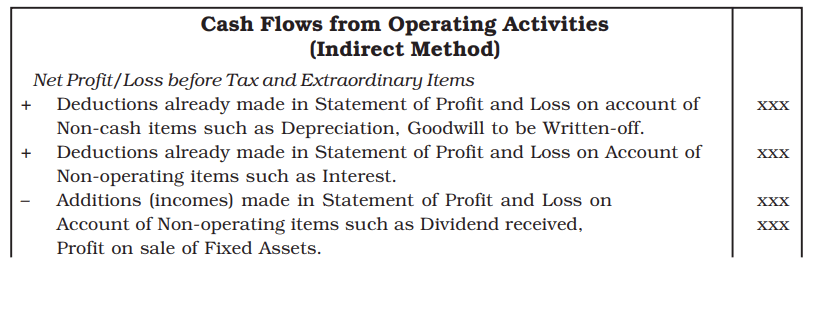

- Indirect method whereby net profit or loss is duly adjusted for the effects of (1) transactions of a non-cash nature, (2) any deferrals or accruals of past/future operating cash receipts, and (3) items of income or expenses associated with investing or financing cash flows. It is important to mention here that under indirect method, the starting point is net profit/loss before taxation and extra ordinary items as per Statement of Profit and Loss of the enterprise. Then this amount is for non-cash items, etc., adjusted for ascertaining cash flows from operating activities.

Accordingly, cash flow from operating activities can be determined using either the Direct method or the Indirect method.The direct method provides information which is useful in estimating future cash flows. But such information is not available under the indirect method. However, in practice, indirect method is mostly used by the companies for arriving at the net cash flow from operating activities. The Chapter deals with preparing cash flow statement using indirect method.

As per AS-4, Contingencies and Events Occurring after the Balance Sheet Date, Proposed dividend is shown in the Notes to Accounts. It will be shown as contingent liability since it becomes a liability after it is declared (approved) by the shareholders. It will be accounted in the books of account after it is declared (approved) by the shareholders in the Annual General Meeting. Since, previous year's Proposed Dividend will be declared (approved) in the current year; previous year's Proposed Dividend will be accounted as dividend payable. Also, declared dividend is paid within 30 days of its declaration therefore; it will be paid within the same financial year.

Briefly, proposed dividend of previous year after declaration (approved) by the shareholders will be debited to surplus i.e., Balance in Statement of Profit and Loss. While preparing cash flow statement, previous year's proposed dividend will be added to Act Profit under operating activities and will be shown under financial activity.

6.6.1 Indirect Method

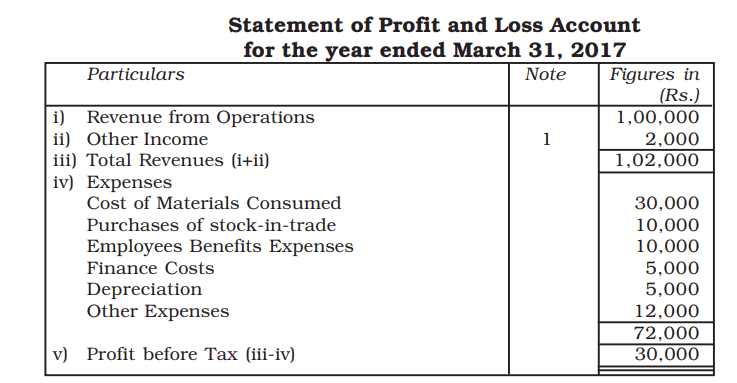

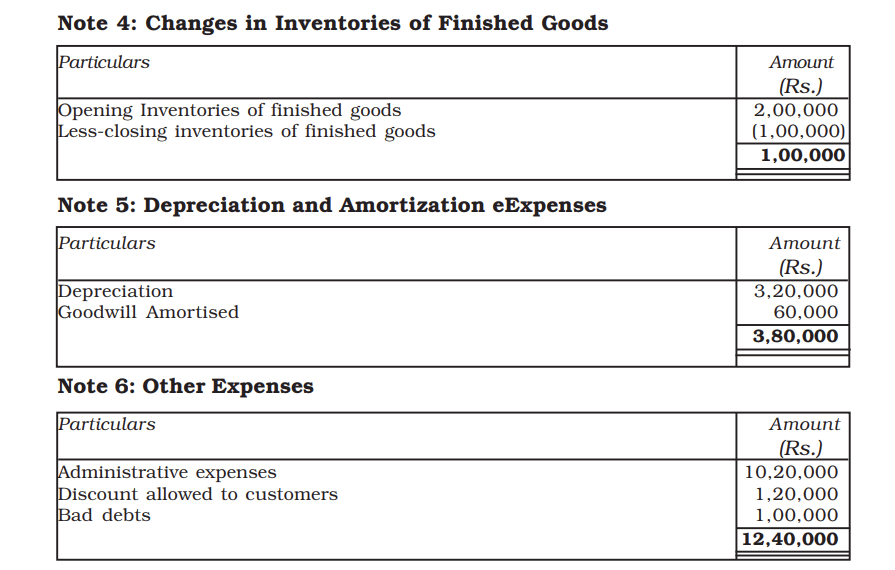

Indirect method of ascertaining cash flow from operating activities begins with the amount of net profit/loss. This is so because statement of profit and loss incorporates the effects of all operating activities of an enterprise. However, Statement of Profit and Loss is prepared on accrual basis (and not on cash basis). Moreover, it also includes certain non-operating items such as interest paid, profit/loss on sale of fixed assets, etc.) and non-cash items (such as depreciation, goodwill written-off, divident declared, etc. Therefore, it becomes necessary to adjust the amount of net profit/loss as shown by Statement of Profit and Loss for arriving at cash flows from operating activities. Let us look at the example :

Note: Other income includes profit on sale of land.

The above Statement of Profit and Loss shows the amount of net profit of Rs. 30,000. This has to be adjusted for arriving cash flows from operating activities. Let us take various items one by one.

1. Depreciation is a non-cash item and hence, Rs. 5,000 charged as depreciation does not result in any cash flow. Therefore, this amount must be added back to the net profit.

2. Finance costs of Rs. 5,000 is a cash outflow on account of financing activity. Therefore, this amount must also be added back to net profit while calculating cash flows from operating activities. This amount of finance cost will be shown as an outflow under the head of financing activities.

3. Other income includes profit on sale of land: It is cash inflow from investing activity. Hence, this amount must be deducted from the amount of net profit while calculating cash flows from operating activities.

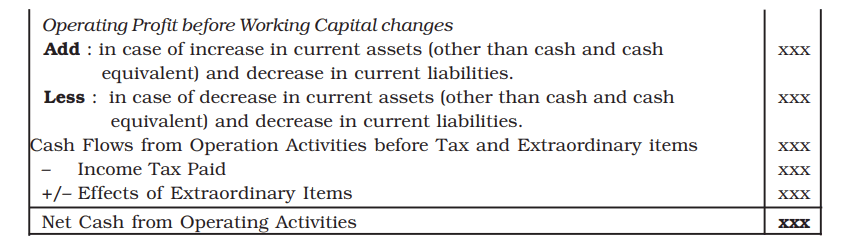

The above example gives you an idea as to how various adjustments are made in the amount of net profit/loss. Other important adjustments relate to changes in working capital which are necessary (i.e., items of current assets and current liabilities) to convert net profit/loss which is based on accrual basis into cash flows from operating activities. Therefore, the increase in current assets and decrease in current liabilities are deducted from the operating profit, and the decrease in current assets and increase in current liabilities are added to the operating profit so as to arrive at the exact amount of net cash flow from operating activities.

As per AS-3, under indirect method, net cash flow from operating activities is determined by adjusting net profit or loss for the effect of :

- Non-cash items such as depreciation, goodwill written-off, provisions,deferred taxes, etc., which are to be added back.

- All other items for which the cash effects are investing or financing cash flows. The treatment of such items depends upon their nature. All investing and financing incomes are to be deducted from the amount of net profits while all such expenses are to be added back. For example, finance cost which is a financing cash outflow is to be added back while other income such as interest received which is investing cash inflow is to be deducted from the amount of net profit. Dividend declared is a financial activity and is therefore added back to net profit and shown as out flow under financial activity.

- Changes in current assets and liabilities during the period. Increase in current assets and decrease in current liabilities are to be deducted while increase in current liabilities and decrease in current assets are to be added up.

Exhibit 6.4 shows the proforma of calculating cash flows from operating activities as per indirect method.

Exhibit 6.4: Proforma of Cash Flows from Operating Activities (Indirect Method)

As stated earlier, while working out the cash flow from operating activities, the starting point is the ‘Net profit before tax and extraordinary items’ and not the ‘Net profit as per Statement of Profit and Loss’. Income tax paid is deducted as the last item to arrive at the net cash flow from operating activities.

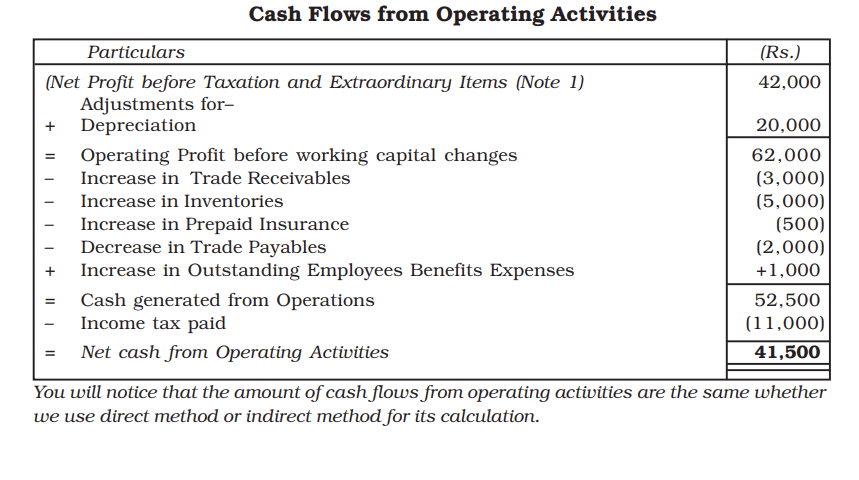

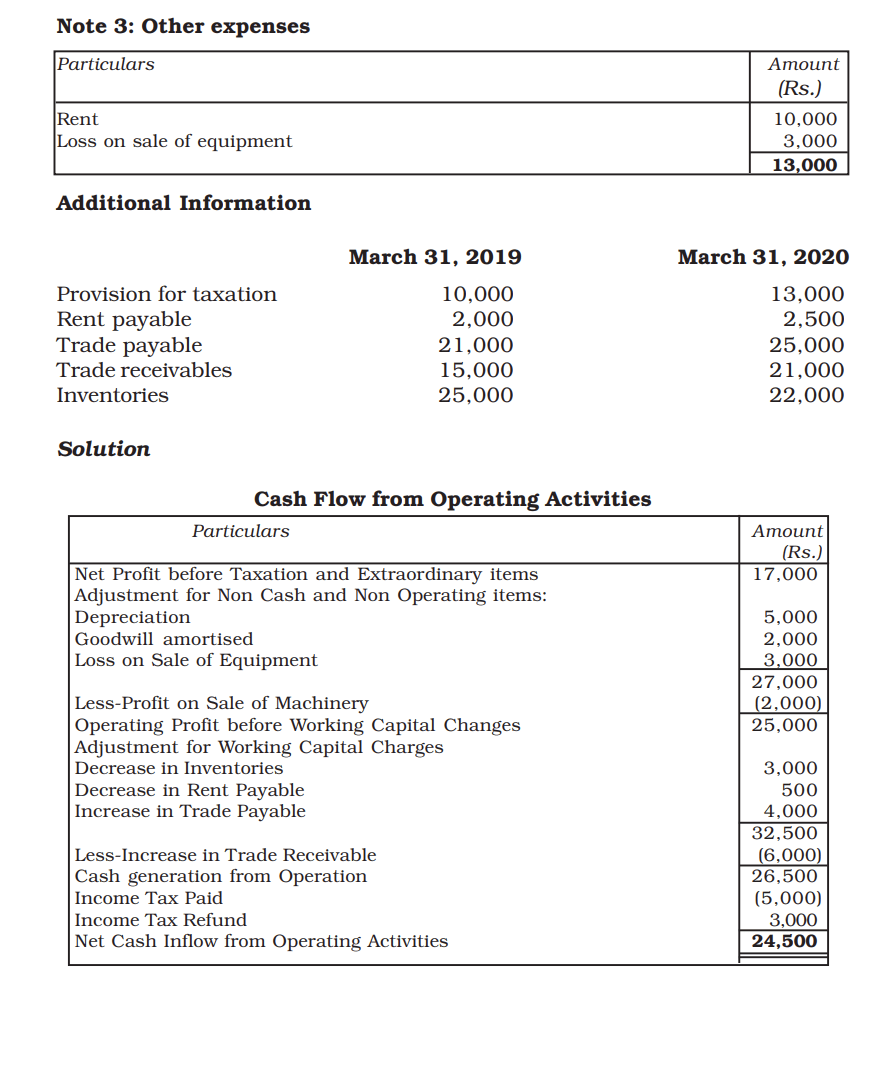

Illustration 2Using the data given in Illustration 1, calculate cash flows from operating activities using indirect method.

Solution:

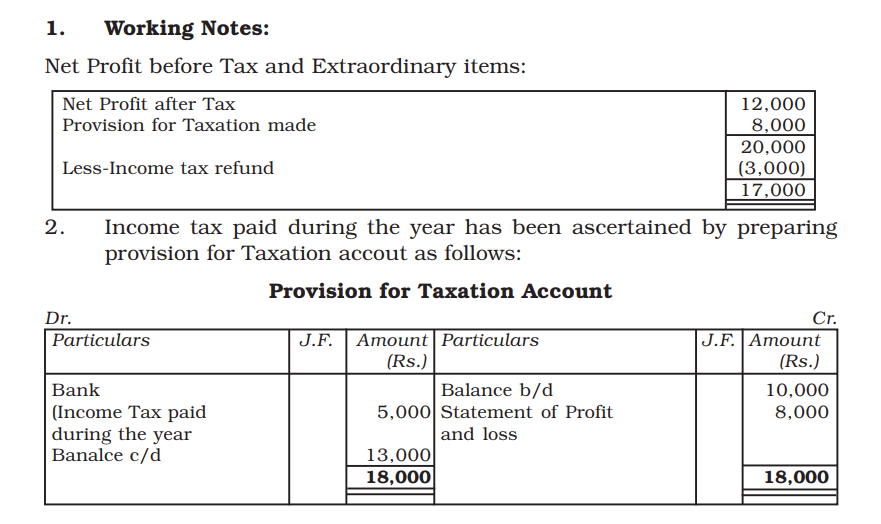

Working Notes :

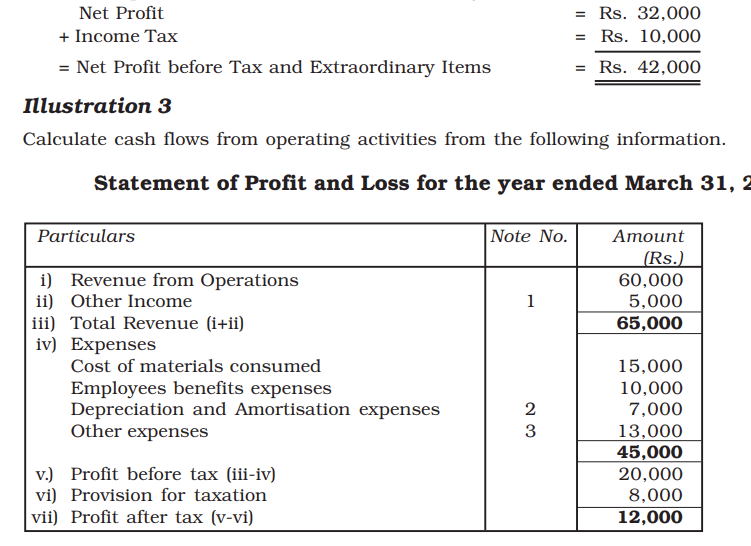

The net profit before taxation and extraordinary items has been worked out as under:

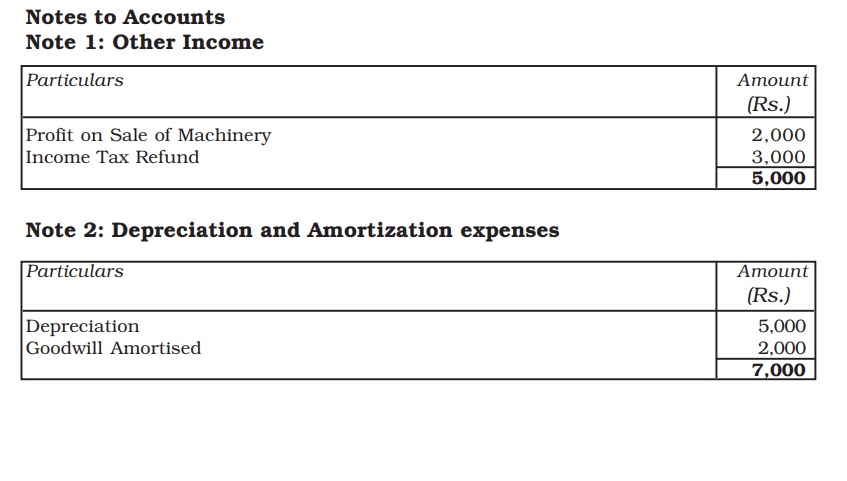

Illustration 4

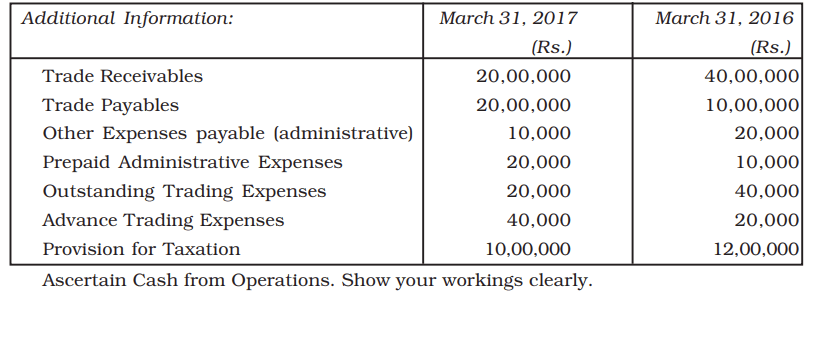

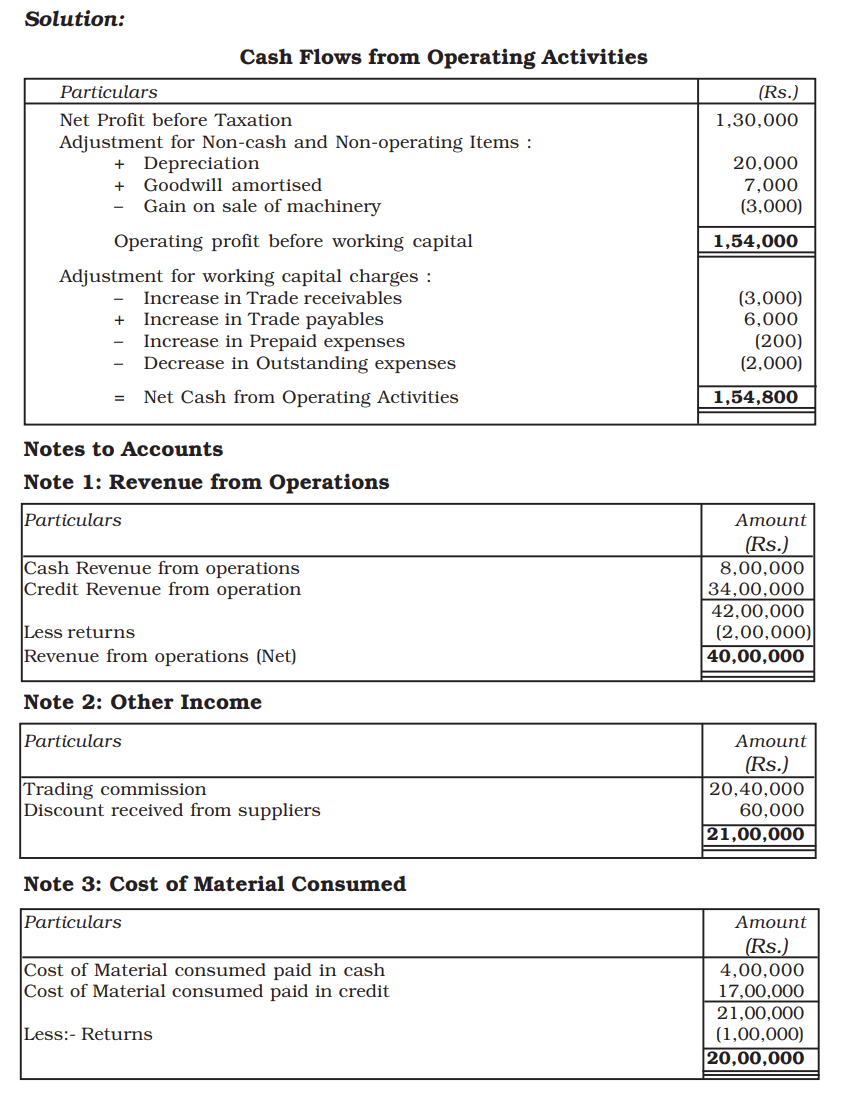

Charles Ltd.,made a profit of Rs. 1,00,000 after charging depreciation of Rs. 20,000 on assets and a transfer to general reserve of Rs. 30,000. The goodwill amortised was Rs. 7,000 and gain on sale of machinery was Rs. 3,000. Other information available to you (changes in the value of current assets and current liabilities) are trade receivables showed an increase of Rs. 3,000; trade payables an increase of Rs. 6,000; prepaid expenses an increase of Rs. 200; and outstanding expenses a decrease of Rs. 2,000. Ascertain cash flow from operating activities.

1. Choose one of the two alternatives given below and fill in the blanks in the following statements:

(a) If the net profits earned during the year is Rs. 50,000 and the amount of debtors in the beginning and the end of the year is Rs. 10,000 and Rs. 20,000 respectively, then the cash from operating activities will be equal to Rs. __________________ (Rs. 40,000/Rs. 60,000)

(b) If the net profits made during the year are Rs. 50,000 and the bills receivables have decreased by Rs. 10,000 during the year then the cash flow from operating activities will be equal to Rs. ________________ (40,000/Rs. 60,000)

(c) Expenses paid in advance at the end of the year are ________________ the profit made during the year (added to/deducted from).

(d) An increase in accrued income during the particular year is ________________ the net profit (added to/deducted from).

(e) Goodwill amortised is ________________ the profit made during the year for calculating the cash flow from operating activities (added to/ deducted from).

(f) For calculating cash flow from operating activities, provision for doubtful debts is ________________ the profit made during the year (added to/ deducted from).

2. While computing cash from operating activities, indicate whether the following items will be added or subtracted from the net profit- if not to be considered, write NC

Items: Treatment(a) Increase in the value of creditors

(b) Increase in the value of patents

(c) Decrease in prepaid expenses

(d) Decrease in income received in advance

(e) Decrease in value of inventory

(f) Increase in share capital

(g) Increase in the value of trade receivables

(h) Increase in the amount of outstanding expenses

(i) Conversion of debentures into shares

(j) Decrease in the value of trade payables

(k) Increase in the value of trade receivables

(l) Decrease in the amount of accrued income.

Sometimes, neither the amount of net profit is specified nor the Statement of profit and loss is given. In such a situation, the amount of net profit can be worked out by comparing the balances of Statement of Profit and Loss given in the comparative balance sheets for two years. The difference is treated as the net profit for the year; and, then, by adjusting it with the amount of provision for tax made during the year (as worked out by comparing the provision for tax balances of two years given in balance sheets), the amount of ‘Net Profit before tax’ can be ascertained (see Illustration 7 and 8).

6.7 Ascertainment of Cash Flow from Investing and Financing ActivitiesThe details of item leading inflows and outflows from investing and financing activities have already been outlined. While preparing the cash flow statement, all major items of gross cash receipts, gross cash payments, and net cash flows from investing and financing activities must be shown separately under the headings ‘Cash Flow from Investing Activities’ and ‘Cash Flow from Financing Activities’ respectively.’

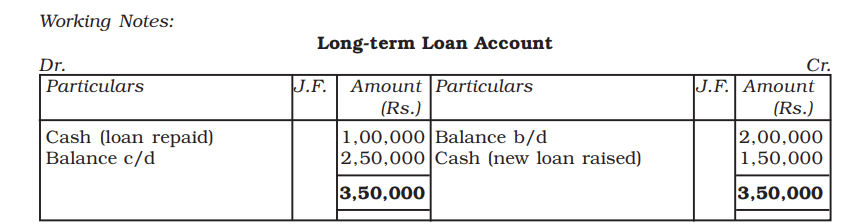

The ascertainment of net cash flows from investing and financing activities have been briefly dealt with in Illustrations 5 and 6.

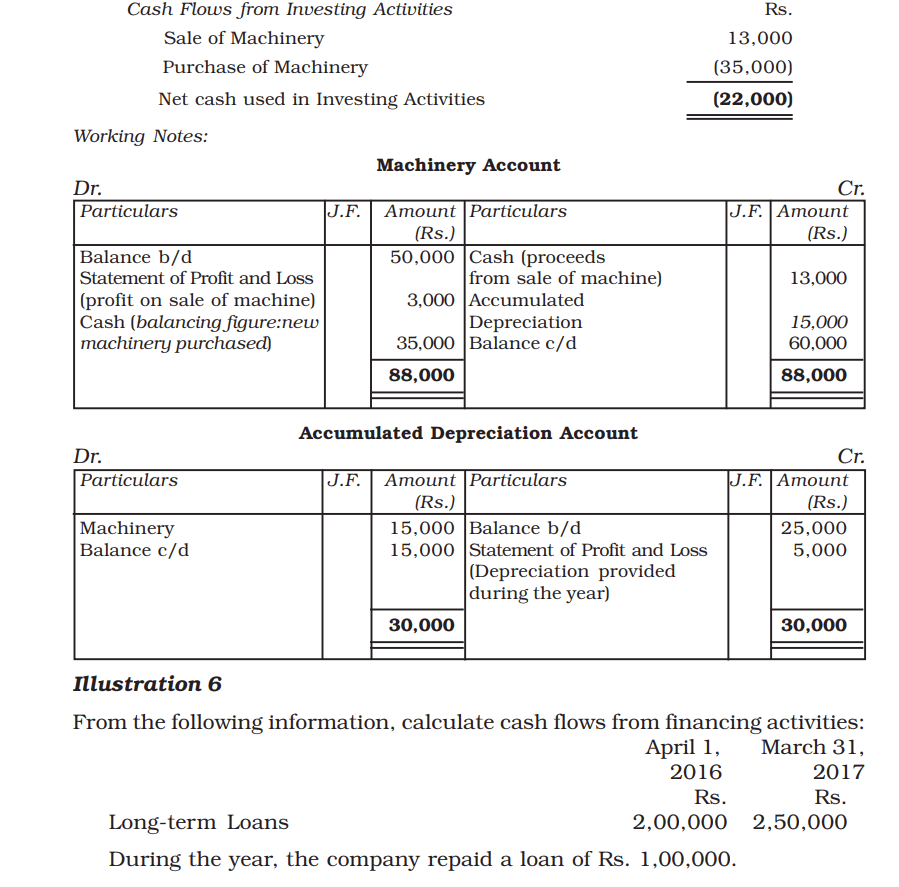

Illustration 5Welprint Ltd. has given you the following information: Rs.

Machinery as on April 01, 2016

50,000

Machinery as on March 31, 2017

60,000

Accumulated Depreciation on April 01, 2016

25,000

Accumulated Depreciation on March 31, 2017

15,000

During the year, a Machine costing Rs. 25,000 with Accumulated Depreciation of Rs. 15,000 was sold for Rs. 13,000.

Calculate cash flow from Investing Activities on the basis of the above information.

Solution:

6.8 Preparation of Cash Flow Statement

As stated earlier cash flow statement provides information about change in the

position of Cash and Cash Equivalents of an enterprise, over an accounting

period. The activities contributing to this change are classified into operating,

investing and financing. The methology of working out the net cash flow (or

use) from all the three activities for an accounting period has been explained

in details and a brief format of Cash Flow Statement has also been given in

Exhibit 6.2. However, while preparing a cash flow statement, full details of

inflows and outflows are given under these heads including the net cash flow

(or use). The aggregate of the net ‘cash flows (or use) is worked out and is

shown as ‘Net Increase/Decrease in cash and Cash Equivalents’ to which the

amount of ‘cash and cash equivalent at the beginning’ is added and thus the

amount of ‘cash and cash equivalents at the end’ is arrived at as shown in

Exhibit 6.2. This figure will be the same as the total amount of cash in hand,

cash at bank and cash equivalants (if any) given in the balance sheet (see

Illustrations 7 to 10). Another point that needs to be noted is that when cash

flows from operating activities are worked out by an indirect method and

shown as such in the cash flow statement, the statement itself is termed as

‘Indirect method cash flow statement’. Thus, the Cash flow statements prepared

in Illustrations 7, 8 and 9 fall under this category as the cash flows from

operating activities have been worked out by indirect method. Similarly, if the

cash flows from operating activities are worked by direct method while preparing

the cash flow statement, it will be termed as ‘direct method Cash Flow

Statement’. Illustration 10 shows both types of Cash Flow Statement. However,

unless it is specified clearly as to which method is to be used, the cash flow

statement may preferably be prepared by an indirect method as is done by

most companies in practice.

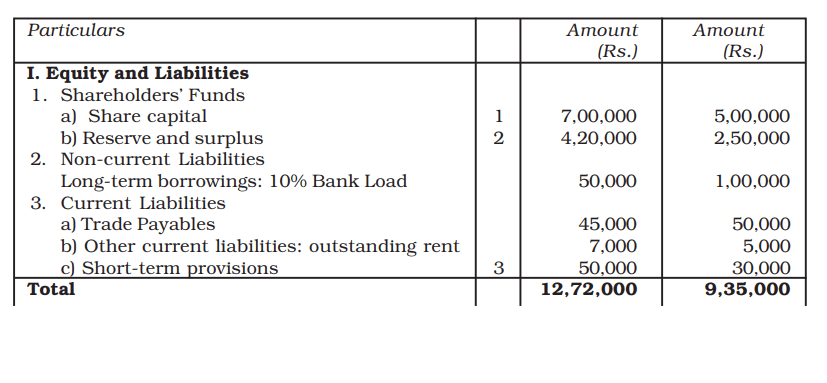

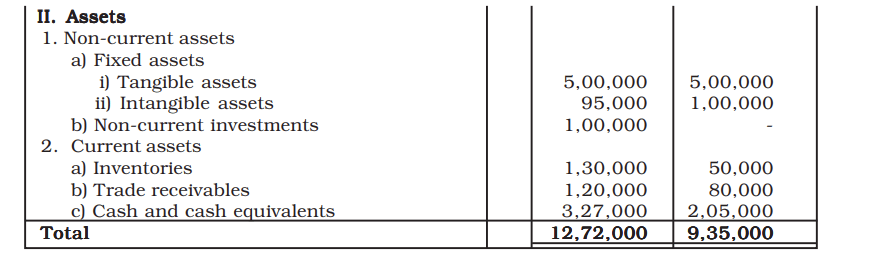

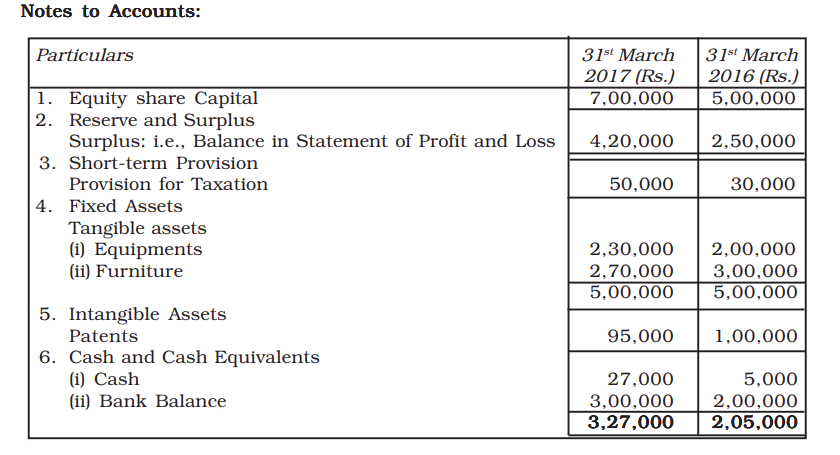

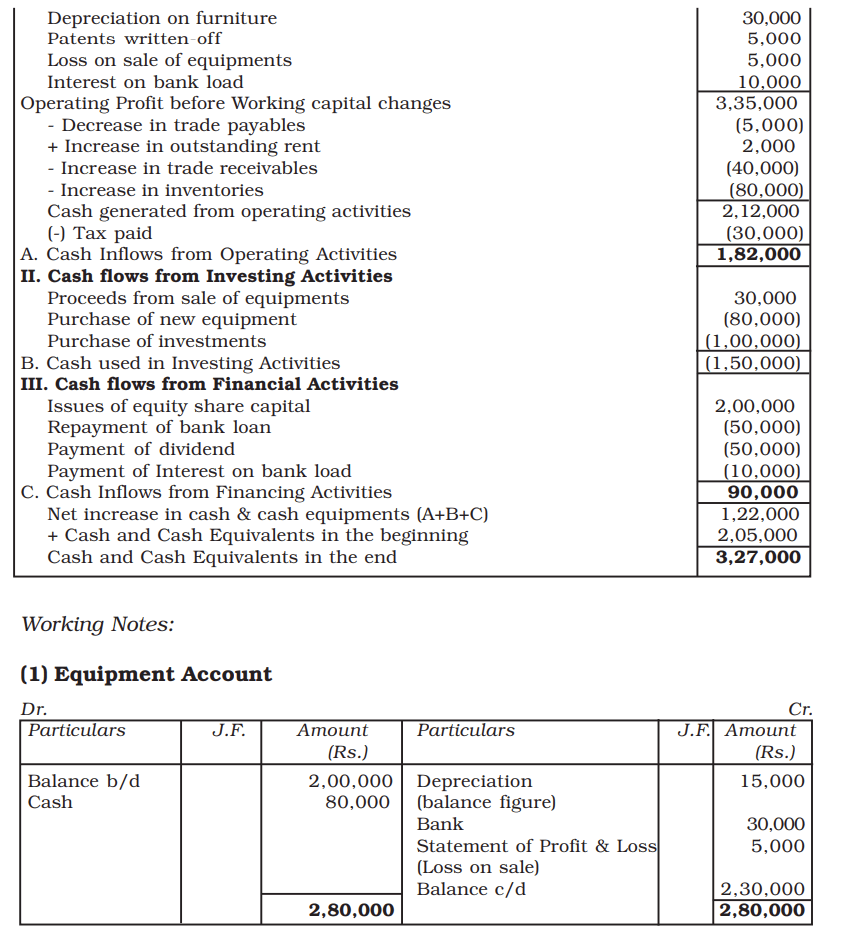

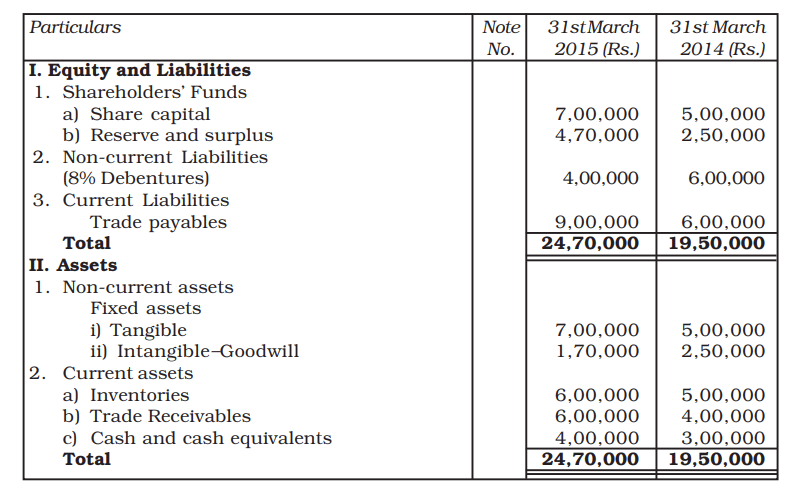

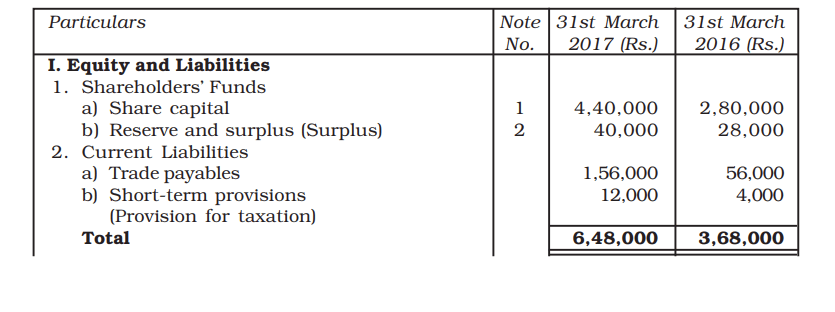

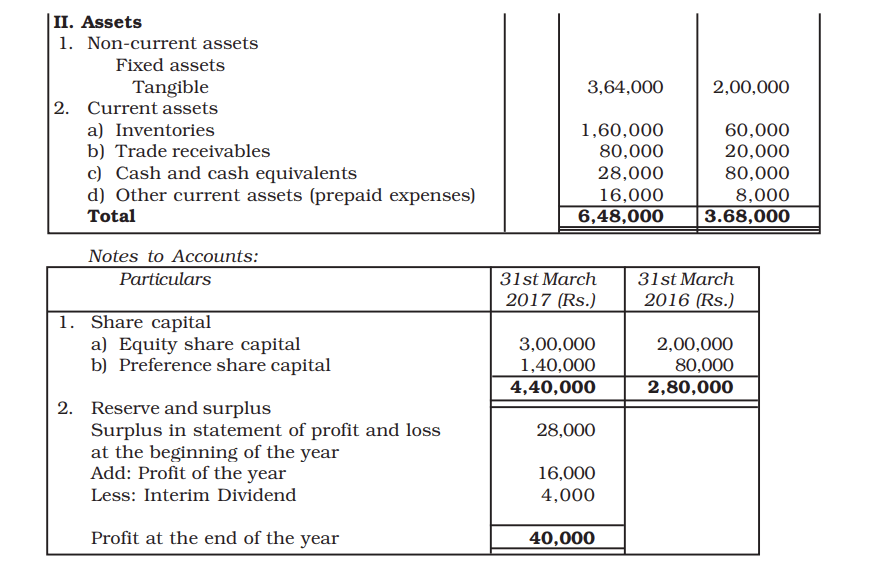

Illustration 7

From the following information, prepare Cash Flow Statement for Pioneer Ltd.

Balance Sheet of Pioneer Ltd., as on March 31, 2017

Additional Information

During the year, equipment costing Rs. 80,000 was purchased. Loss on sale

of equipment amounted to Rs. 5,000. Depreciation of Rs. 15,000 and Rs.

3,000 charged on equipments and furniture. Loan Rs. 50,000 was repaid on

31.03.2017. Proposed dividend for the year 2015-16 was Rs. 50,000.

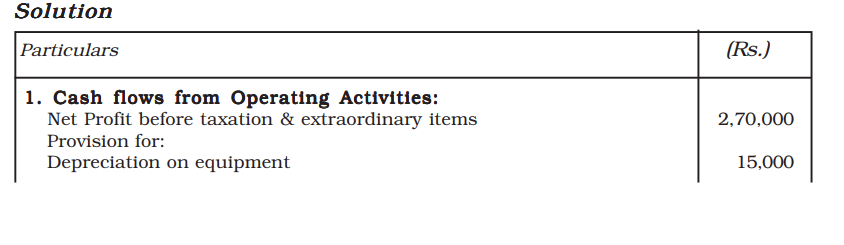

Cash Flow Statement

(2) Patents of Rs. 5,000 (i.e., Rs. 1,00,000-Rs. 95,000) were written-off during the year, and depreciation on furniture was Rs. 30,000. (Rs. 3,00,000-Rs. 2,70,000)

(3) It is assumed that dividend of Rs. 50,000 and tax of Rs. 30,000 provided in 2015-2016 has been paid during the year 2016-17. Hence, proposed dividend and provision for tax during the year amounts to Rs. 70,000 and Rs. 50,000 respectively.

Cash Flow Statement

Cash Flow Statement

Additional information:

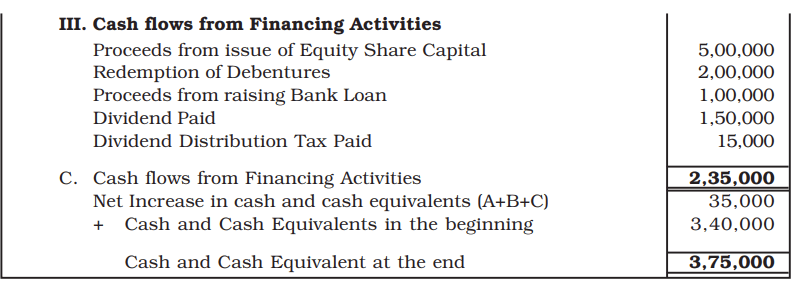

1. Proposed dividend 2016-17 is Rs. 2,25,000 and for 2015-16 is Rs. 1,50,000.

2. Income tax paid during the year includes Rs. 15,000 on account of dividend tax.

3. Land and building book value Rs. 1,50,000 was sold at a profit of 10%.

4. The rate of depreciation on plant and machinery is 10%.

5. 9% debentures redeemed on April 2017, 5% bank loan was opted on March 31, 2017.

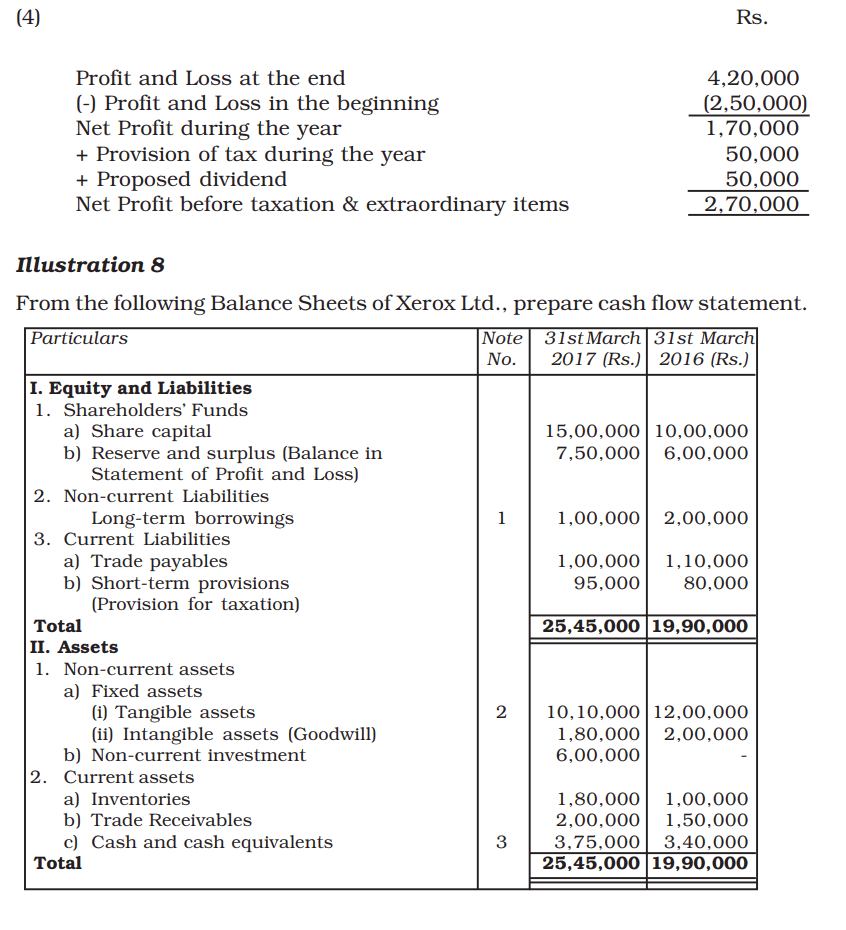

(2) Net profit earned during the year after tax and dividend

= Rs. 7,50,000 – 6,00,000 = Rs. 1,50,000

(3) Net profit before tax

= Net profit earned during the year after tax and dividend + Provision for tax made + Declared Dividend

= Rs. 1,50,000 + Rs. 95,000 (See provision for taxation)+ Rs. 1,50,000

= Rs. 3,95,000

Equity Share Capital Account

Illustration 9

Illustration 9

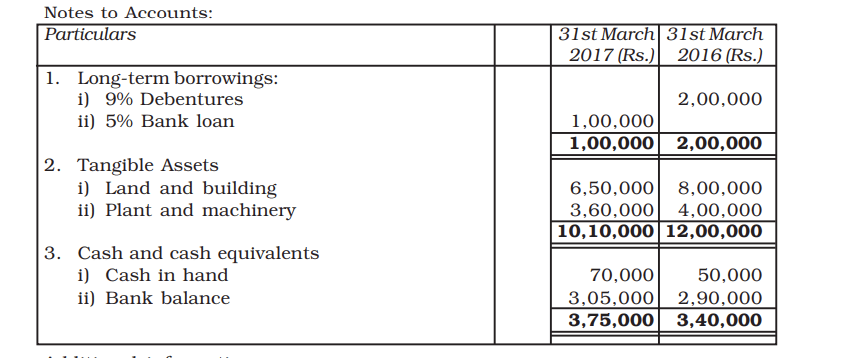

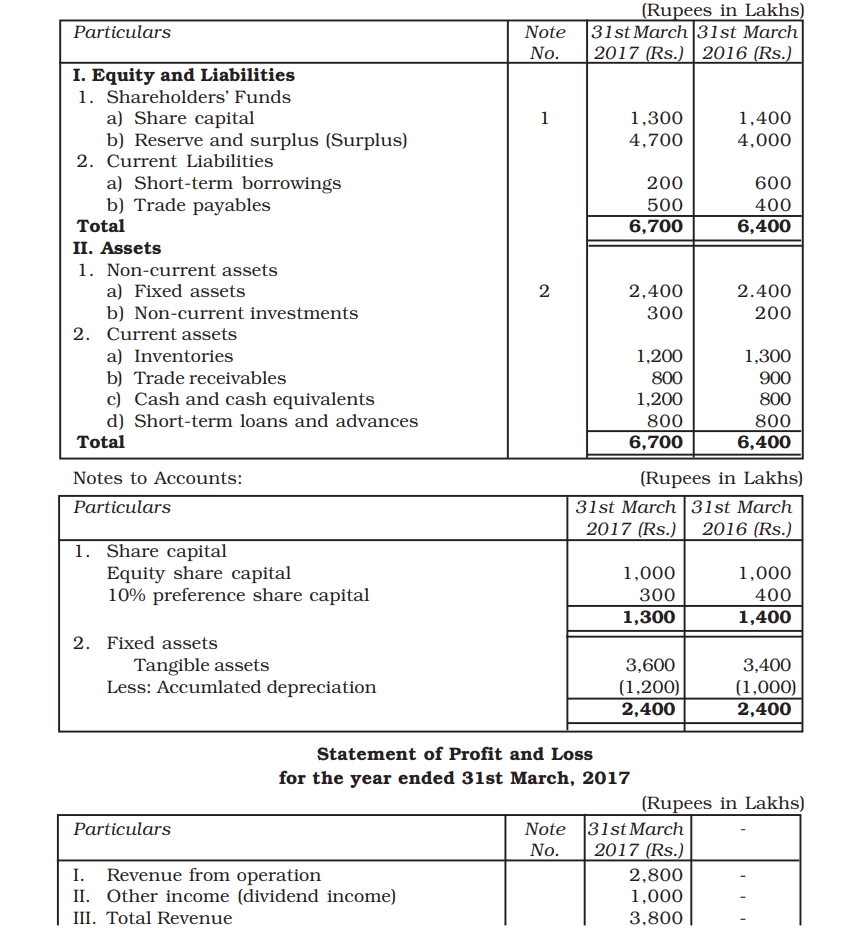

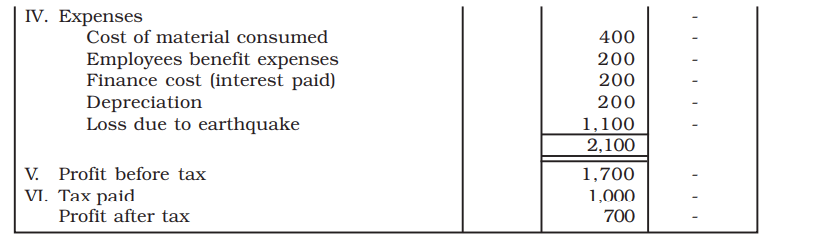

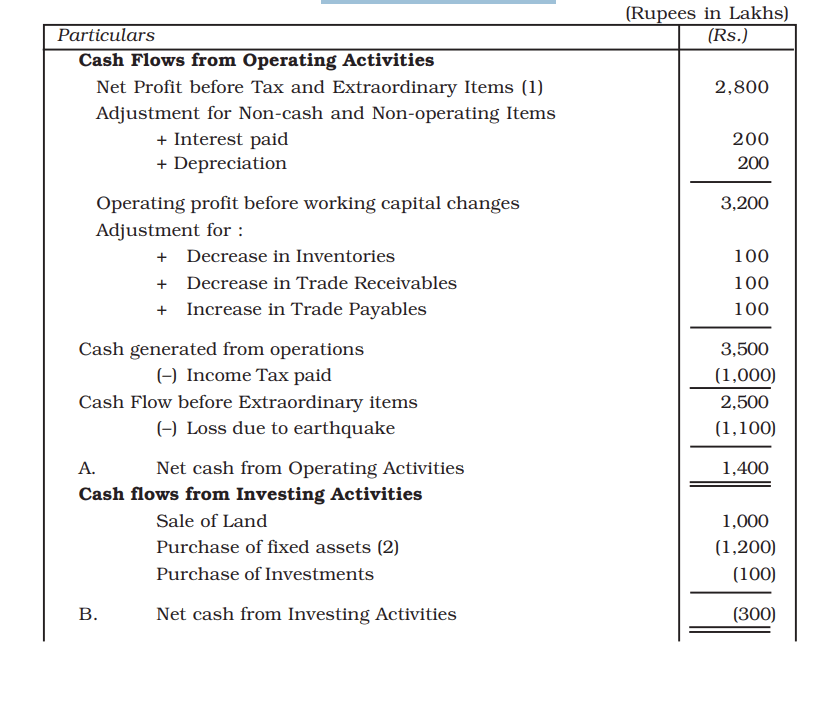

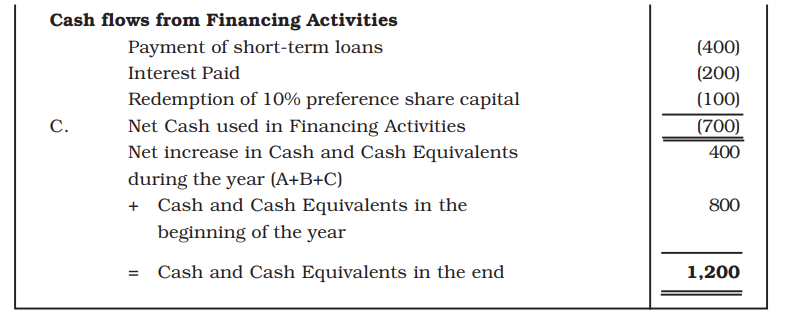

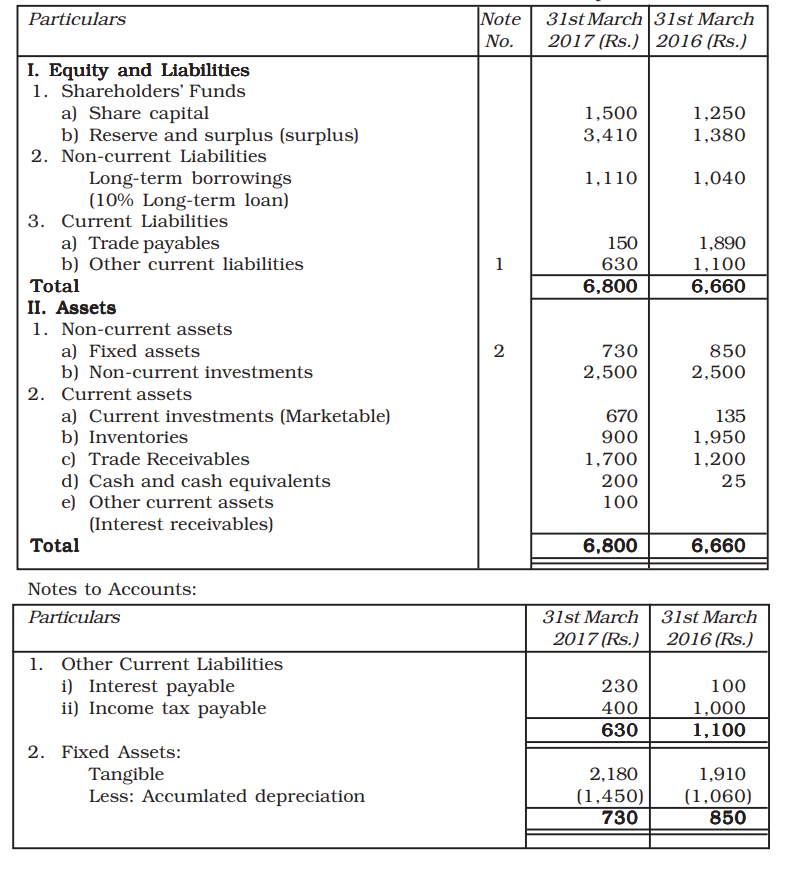

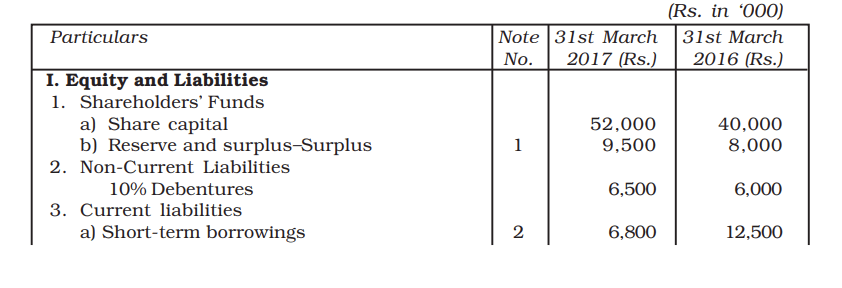

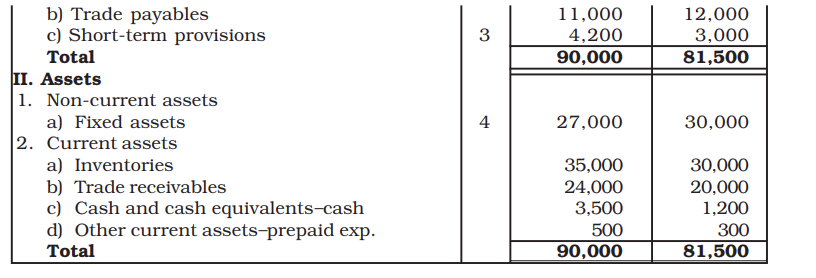

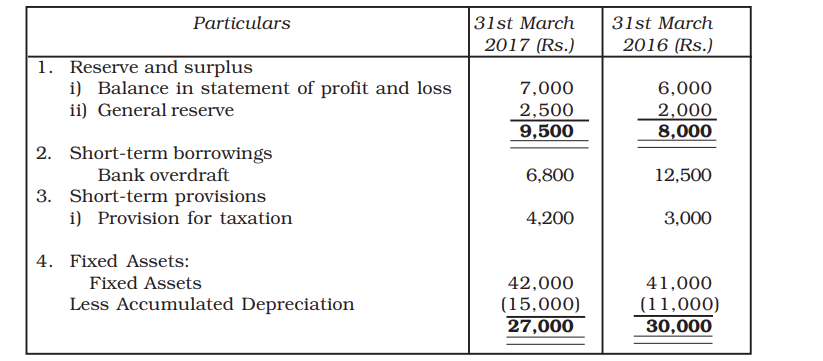

From the following information of Oswal Mills Ltd., prepare cash flow statement:

Balance Sheet of Oswal Mills

as on 31st March, 2016 and 2017

Cash Flow Statement

Additional information:

1. No dividend paid by the company during the current financial year.

2. Out of fixed assets, land worth Rs. 1,000 Lakhs was sold at this amount.

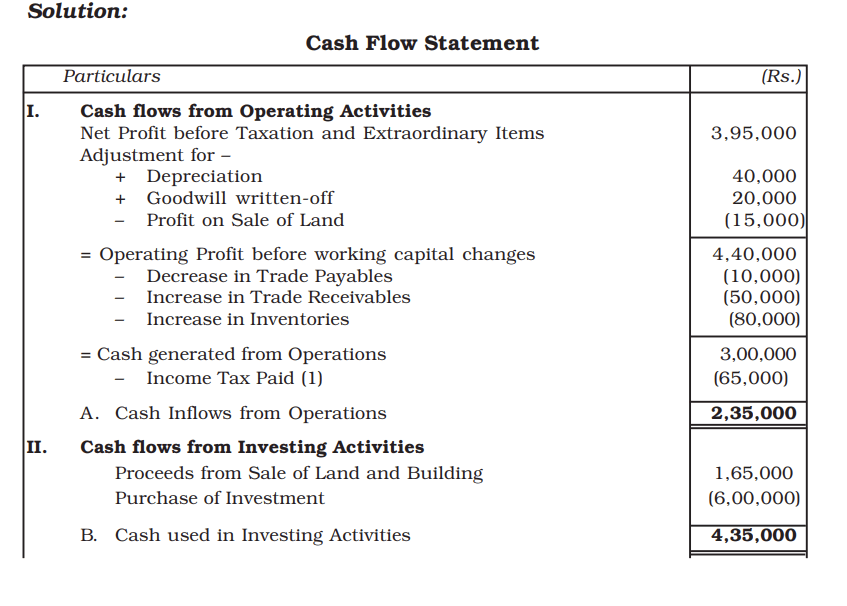

Solution:Cash Flow Statement

Working Notes:

(Rupees in Lakhs)

(

Working Notes:

(Rupees in Lakhs)

(1) Net Profit before Tax and Extraordinary Items = Rs. 700 + Rs. 1,100 + Rs. 1,000

= Rs. 2,800

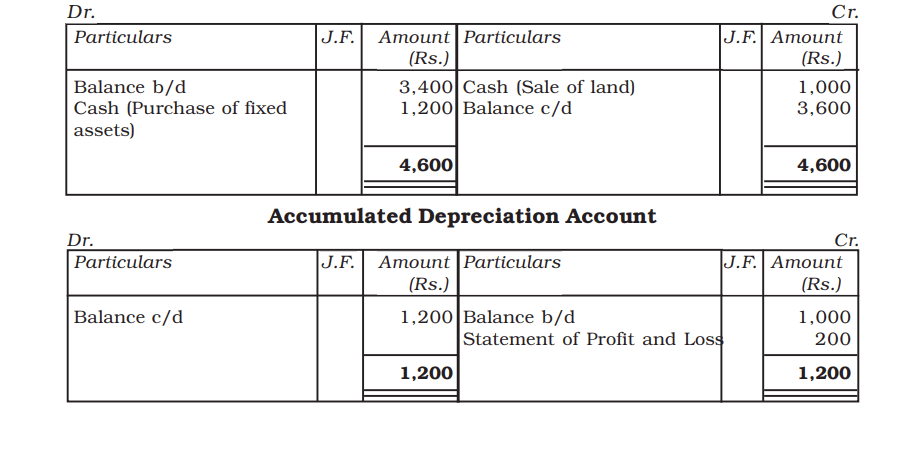

(2) Fixed Assets Account Illustration 10

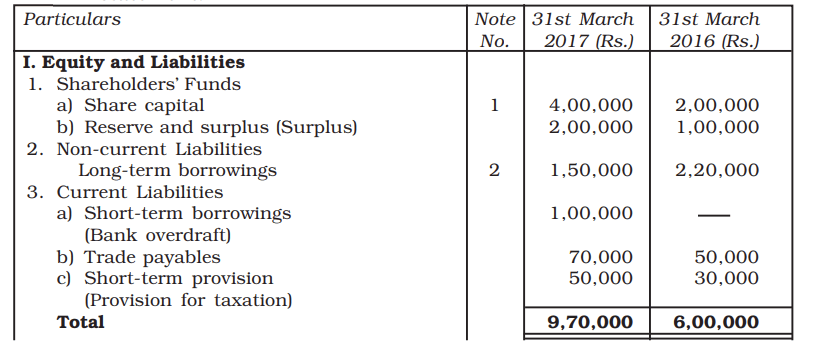

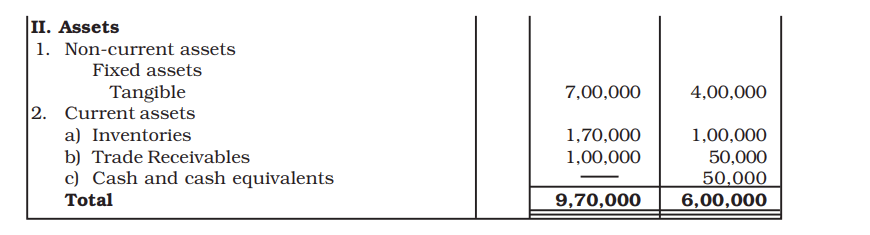

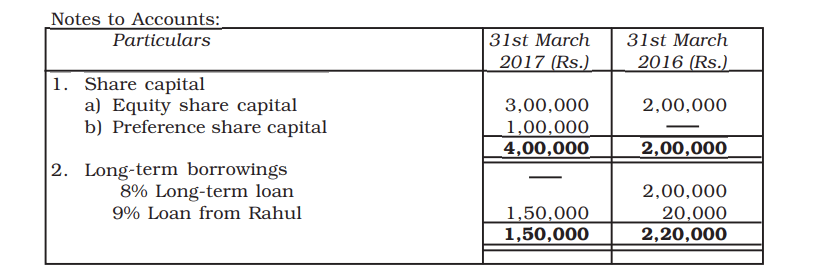

Illustration 10

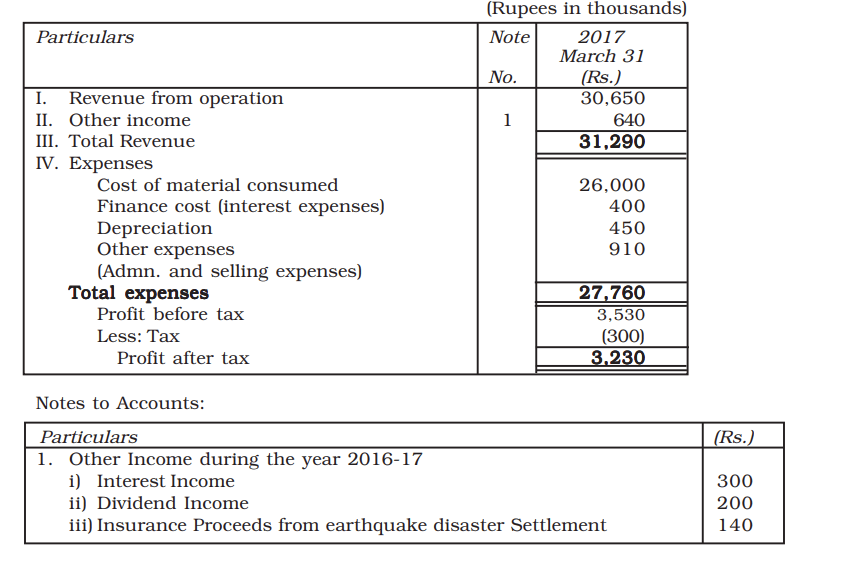

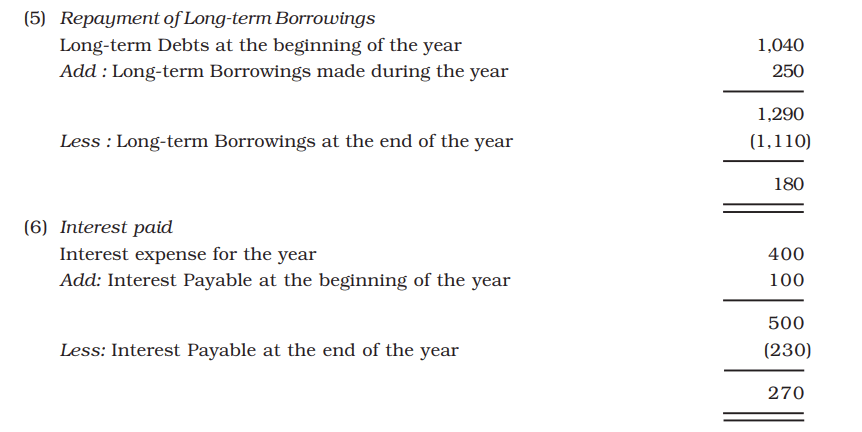

From the following information of Banjara Ltd., prepare a cash flow statement:

Statement of Profit and Loss for the year ended

31 March, 2017

Additional Information:

(Rs. ’000)

(i) An amount of Rs. 250 was raised from the issue of share capital and a further Rs. 250 was raised from long-term borrowings.

(ii) Interest expense was Rs. 400 of which Rs. 170 was paid during the period. Rs. 100 relating to interest expense of the prior period was also paid during the period.

(iii) Dividends paid were Rs. 1,200.

(iv) 10% loan of Rs. 70,00,000 was obtained in March 31, 2017

(v) During the period, the enterprise acquired Fixed Assets for Rs. 350. The payment was made in cash.

(vi) Plant with original cost of Rs. 80 and accumulated depreciation of Rs. 60 was sold for Rs. 20.

(vii) Trade Receivables and Trade Payables include amounts relating to credit sales and credit purchases only.

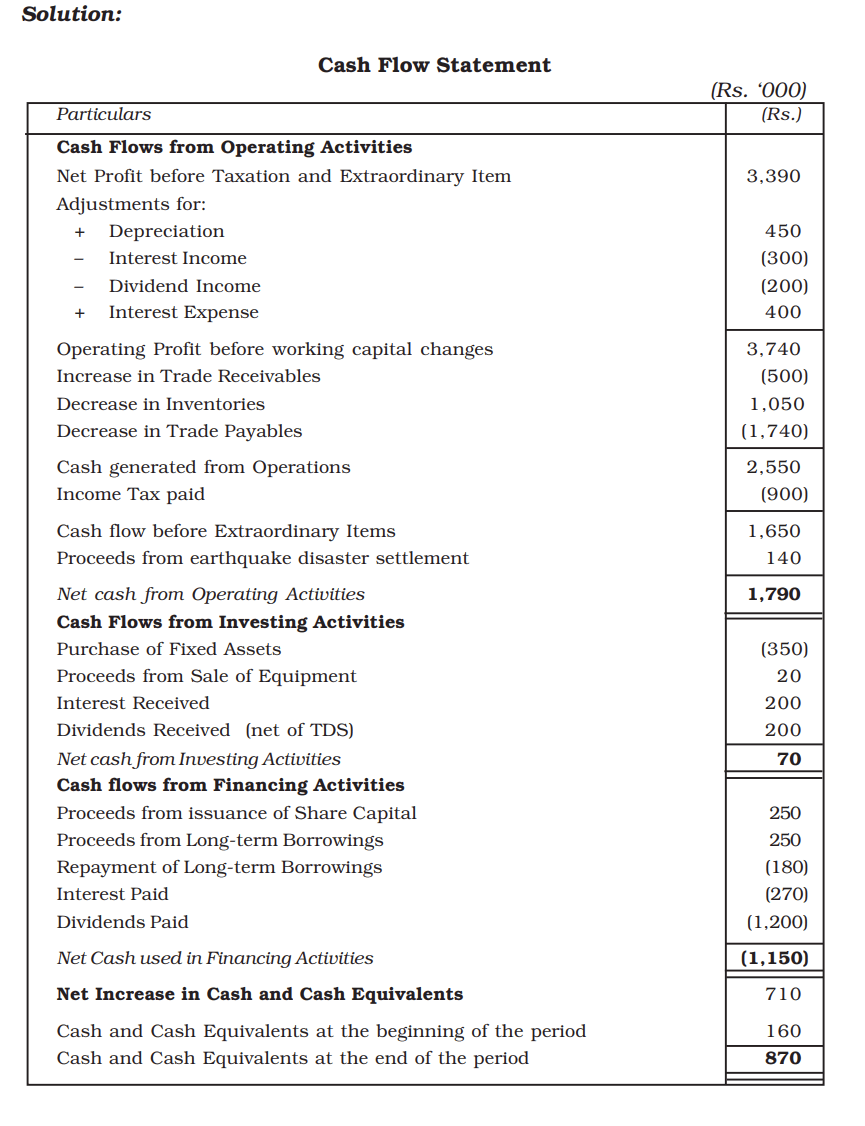

Cash Flow Statement

Note: Cash flow statement is prepared from statement of profit and loss. Hence, dividend paid will be adjusted in financing activity only.

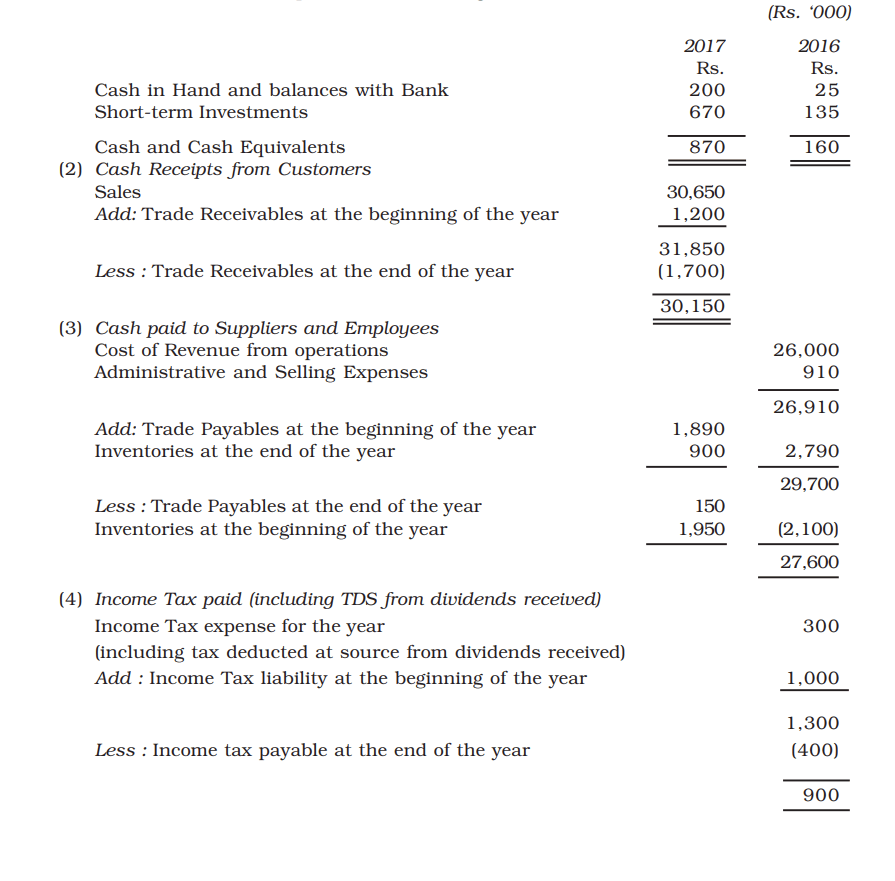

Working Notes: (1) Cash and Cash EquivalentsCash and Cash Equivalents consist of cash in hand and balances with banks, and investments in money-market instruments. Cash and Cash Equivalents included in the Cash Flow Statement comprise of the following balance sheet amounts.

Cash Flow Statement

Cash Flow Statement

Terms Introduced in the Chapter

Terms Introduced in the Chapter- Cash

- Cash Equivalents

- Cash Inflows

- Cash Outflows

- Non-cash item

- Cash Flow Statement

- Operating Activities

- Investing Activities

- Financing Activities

- Accounting Standard-3

- Extraordinary Items

Cash Flow Statement: The Cash Flow Statement helps in ascertaining the liquidity of an enterprise. Cash Flow Statement is to be prepared and reported by Indian companies according to AS-3 notified as per Companies Act 2013. The cash flows are categorised into flows from operating, investing and financing activities. This statement helps the users to ascertain the amount and certainty of cash flows to be generated by company

Questions for Practice

Short Answer Questions- What is a Cash flow statement?

- How are the various activities classified (as per AS-3 revised) while

- preparing cash flow statement?

- State the objectives of cash flow statement.

- What are the objectives of preparing cash flow statement?

- State the meaning of the terms: (i) Cash Equivalents, (ii) Cash flows.

- Prepare a format of cash flow from operating activities.

- State clearly what would constitute the operating activities for each of

- the following enterprises:

(i) Hotel

(ii) Film production house

(iii) Financial enterprise

(iv) Media enterprise

(v) Steel manufacturing unit

(vi) Software development business unit.

8. “The nature/type of enterprise can change altogether the category into which a particular activity may be classified.” Do you agree? Illustrate your answer.

Long Answer Questions1. Describe the procedure to prepare Cash Flow Statement.

2. Describe “Indirect” method of ascertaining Cash Flow from operating activities.

3. Explain the major Cash Inflows and outflows from investing activities.

4. Explain the major Cash Inflows and outflows from financing activities.

Numerical Questions1. Anand Ltd., arrived at a net income of Rs. 5,00,000 for the year ended March 31, 2017. Depreciation for the year was Rs. 2,00,000. There was a profit of Rs. 50,000 on assets sold which was transferred to Statement of Profit and Loss account. Trade Receivables increased during the year Rs. 40,000 and Trade Payables also increased by Rs. 60,000. Compute the cash flow from operating activities by the indirect approach.

Cash Flow Statement

[Ans.: Rs. 6,70,000]

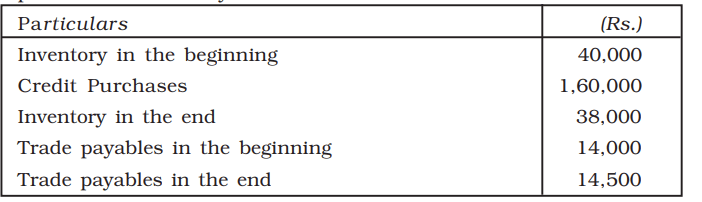

2. From the information given below you are required to calculate the cash paid for the inventory:

[Ans.: Rs. 1,59,500]

3. For each of the following transactions, calculate the resulting cash flow and state the nature of cash flow, viz., operating, investing and financing.

(a) Acquired machinery for Rs. 2,50,000 paying 20% by cheque and executing a bond for the balance payable.

(b) Paid Rs. 2,50,000 to acquire shares in Informa Tech. and received a dividend of Rs. 50,000 after acquisition.

(c) Sold machinery of original cost Rs. 2,00,000 with an accumulated depreciation of Rs. 1,60,000 for Rs. 60,000.

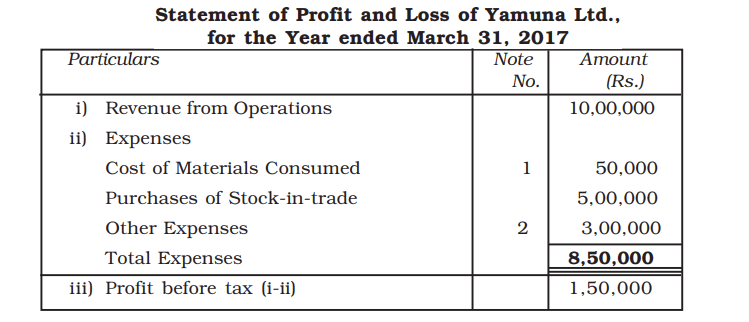

[Ans.: (a) Rs. 50,000 investing activity (outflow); (b) Rs. 2,00,000 investing activity (outflow); (c) Rs. 60,000 investing activity (inflow)].4. The following is the Profit and Loss Account of Yamuna Limited:

Additional information:

(i) Trade receivables decrease by Rs. 30,000 during the year.

(ii) Prepaid expenses increase by Rs. 5,000 during the year.

(iii) Trade payables increase by Rs. 15,000 during the year.

(iv) Outstanding expenses payable increased by Rs. 3,000 during the year.

(v) Other expenses included depreciation of Rs. 25,000.

Compute net cash from operations for the year ended March 31, 2017 by the indirect method.

[Ans.: Cash from operations Rs. 2,18,000].

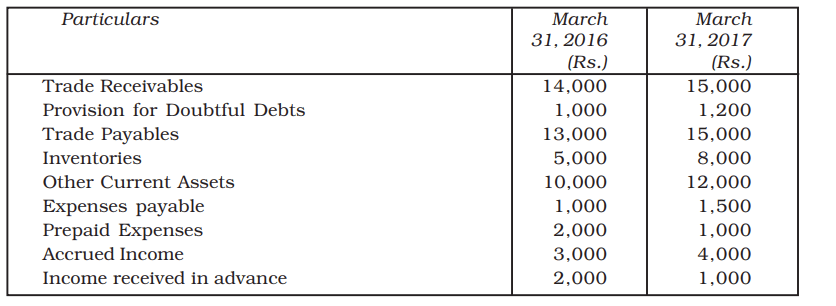

5. Compute cash from operations from the following figures:

(i) Profit for the year 2016-17 is a sum of Rs. 10,000 after providing for depreciation of Rs. 2,000.

(ii) The current assets and current liabilities of the business for the year ended March 31, 2016 and 2015 are as follows:

[Ans.: Cash from operations: Rs. 7,700].

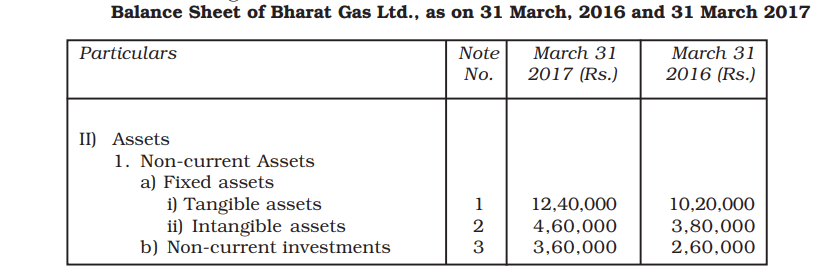

6. From the following particulars of Bharat Gas Limited, calculate Cash Flows from Investing Activities. Also show the workings clearly preparing the ledger accounts:

Notes: 1 Tangible assets = Machinery

2 Intangible assets = Patents

Cash Flow Statement

Additional Information:

Additional Information:

(a) Patents were written-off to the extent of Rs. 40,000 and some Patents were sold at a profit of Rs. 20,000.

(b) A Machine costing Rs. 1,40,000 (Depreciation provided thereon Rs. 60,000) was sold for Rs. 50,000. Depreciation charged during the year was Rs. 1,40,000.

(c) On March 31, 2016, 10% Investments were purchased for Rs. 1,80,000 and some Investments were sold at a profit of Rs. 20,000. Interest on Investment was received on March 31, 2017.

(d) Amartax Ltd., paid Dividend @ 10% on its shares.

(e) A plot of Land had been purchased for investment purposes and let out for commercial use and rent received Rs. 30,000.

[Ans.: Rs. 5,24,000].

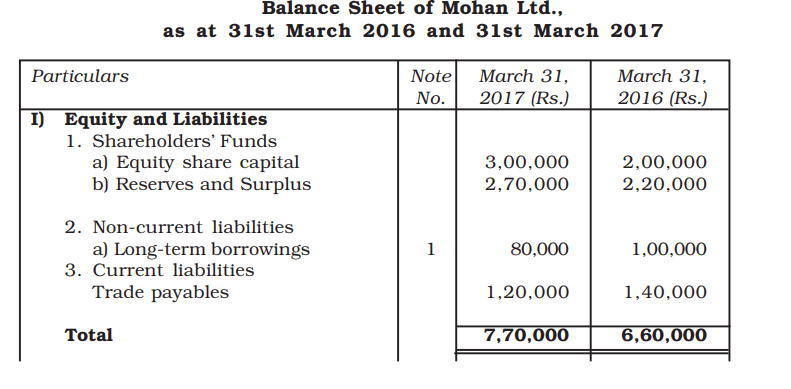

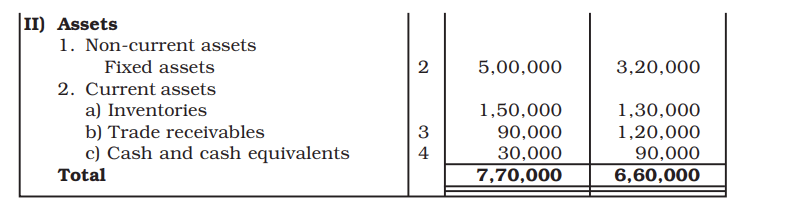

7. From the following Balance Sheet of Mohan Ltd., prepare cash flow Statement:

Additional Information:

Additional Information:

Machine Costing Rs. 80,000 on which accumulated depreciation was Rs. 50,000 was sold for Rs. 20,000. 9% bank loan Rs. 20,000 was repaid on March 31, 2017. Proposed dividend for the year 2015-16 was Rs. 60,000.

Rs.[Ans.: Cash flow from Operating Activities 1,89,000

Cash flow from Investing Activities 2,60,000

Cash flow from Financing Activities 11,000].

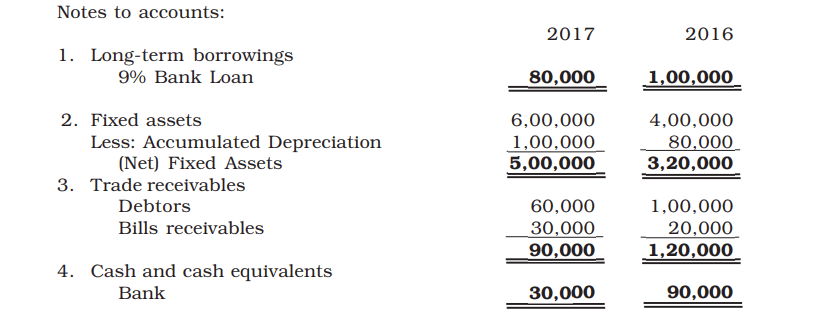

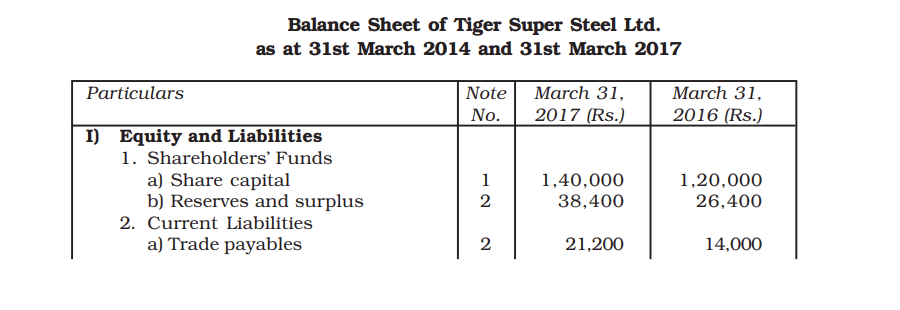

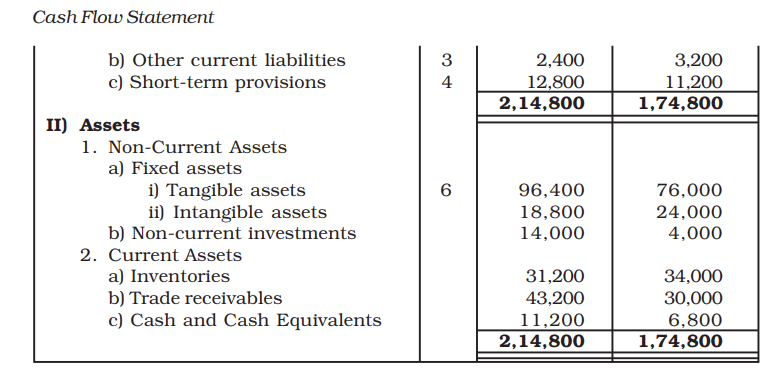

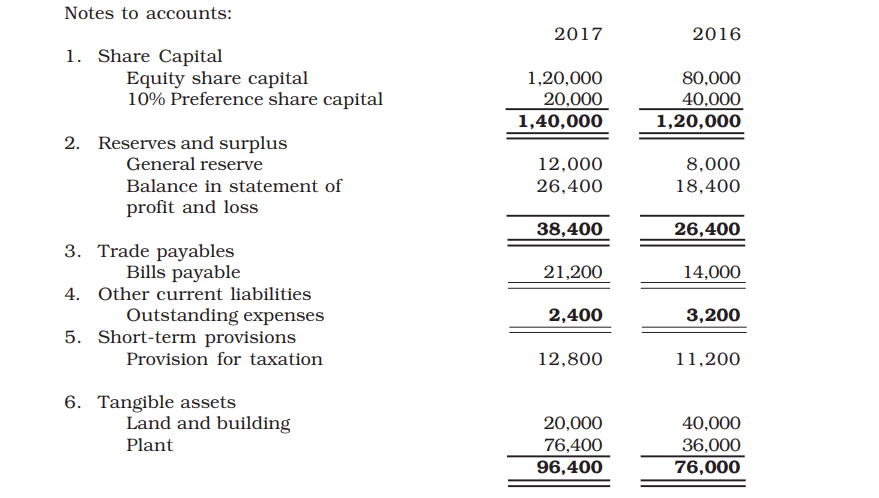

8. From the following Balance Sheets of Tiger Super Steel Ltd., prepare Cash Flow Statement:

Additional Information:

*Proposed dividend for 2016-17 is Rs. 15,600 and for 2015-16 is Rs. 11,200.

Depreciation Charged on Land & Building Rs. 20,000, and Plant Rs. 10,000 during the year. Proposed dividend for 2016-17 Rs. 15,600 and 2015-16 Rs. 11,200

[Ans.: Cash flow from Operating Activities Rs. 56,000

Cash flow from Investing Activities Rs. 60,400

Cash flow from Financing Activities Rs. 8,800].

9. From the following information, prepare cash flow statement:

Additional Information:

Additional Information:

Depreciation Charged on Plant amounted to Rs. 80,000. Rs.

[Ans.: Cash inflow from Operating Activities 4,28,000

Cash inflow from Investing Activities 2,80,000

Cash inflow from Financing Activities 48,000].

10. From the following Balance Sheet of Yogeta Ltd., prepare cash flow statement: Cash Flow Statement

Cash Flow Statement

Additional Information:

Additional Information:

Net Profit for the year after charging Rs. 50,000 as Depreciation was Rs. 1,50,000. Dividend paid on Share was Rs. 50,000, Tax Provision created during the year amounted to Rs. 60,000. 8% loan was repaid on March 31, 2017 and an additional 9% loan of Rs. 1,30,000 was obtained from Rahul on April 01, 2016.

[Ans.: Cash from Operating Activities Rs.1,49,500

Cash from Investing Activities Rs.13,50,000

Cash from Financing Activities Rs.1,50,000].

11. Following is the Balance sheet of Garima Ltd., prepare cash flow statement.

Additional Information:

Additional Information:

1. Depreciation charged during the year Rs. 32,000

[Ans.: Cash flow from Operating Activities Rs. 12,000

Cash flow from Investing Activities Rs. 1,96,000

Cash flow from Financing Activities Rs.1,56,400].

12. From the following Balance Sheet of Computer India Ltd., prepare cash flow statement.

Cash Flow Statement

Cash Flow Statement

Notes to Accounts:

Notes to Accounts:

Additional Information:

Additional Information:

Proposed dividend for the year 2015-16 is Rs. 2,50,00,000

[Ans.: Net Cash from Operating Activities Rs. 2,100

Net Cash from Investing Activities Rs. 1,000

Net Cash from Financing Activities Rs. 4,900].

Answers to Test your UnderstandingTest your Understanding – I

Answer :

a) Operating activities - 3, 6, 7, 10, 13, 15, 19, 20, 23, 24, 27;

b) Investing activities - 1, 5, 8, 11, 12, 16, 17, 21, 22

c) Financing activities - 2, 4, 9, 14, 18, 25, 26, 28, 29;

d) Cash equivalents - 30, 31, 32, 33.

Test your Understanding – II Answers: (a) 40,000, (b) 60,000, (c) deducted from, (d) deducted from, (e) added to, (f) added toAnswers: 1. +, 2. NC, 3. +, 4. –, 5. +, 6. NC, 7. –, 8 +, 9. NC, 10 –, 11 –, 12 +