If the monopolist firm of Exercise 3, was a public sector firm. The government set a rule for its manager to accept the government fixed price as given (i.e. to be a price taker and therefore behave as a firm in a perfectly competitive market), and the government decide to set the price so that demand and supply in the market are equal. What would be the equilibrium price, quantity and profit in this case?

If the government sets a rule for the public sector firm to accept the fixed price then the monopoly firm will start behaving like a perfectly competitive firm and will become price taker. In such case the firm will earn only normal and no economic profit.

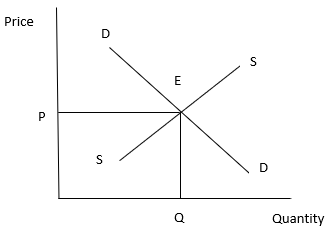

Given below is the graphic presentation of demand and supply at the equilibrium price P(fixed by government) and quantity Q